A few years ago, I stumbled onto something called the “STR Loophole.”

Many real estate investors are missing out on one of the most powerful tax-saving strategies: the short-term rental loophole, also known as the short-term rental tax loophole. I used it to deduct tens of thousands in Airbnb losses last year—without needing to qualify as a real estate professional.

Honestly, I thought it sounded gimmicky. Like one of those TikTok finance bros talking about offshore trusts or renting your car to your LLC.

But this one? It’s real. It’s in the IRS code. And if you’re running short-term rentals — even just one — you might be able to legally use your losses to wipe out active income.

No REPS. No 750-hour tracking. No full-time landlord grind.

Just one short-term rental and the right setup.

Let’s break it down.

What Is the Short Term Rental Loophole?

The Short Term Rental Loophole is a legit tax strategy that lets you treat short-term rental income as non-passive — without having to qualify as a Real Estate Professional.

Normally, real estate is considered passive income. That means even if you lose money (on paper), you can’t use those losses to offset your W-2 income or business profits… unless you qualify for REPS.

But the IRS makes an exception for short-term rentals — if they meet certain conditions.

How It Works (In Plain English)

The key factor is average stay length.

If your property is rented out with an average stay of 7 days or less, the IRS considers it an active trade or business, not passive real estate.

Now, that doesn’t automatically make your losses deductible against your active income. You still have to meet material participation requirements (more on that below). But here’s the kicker:

👉 You do not need to qualify for REPS.

👉 You do not need to hit 750 hours.

👉 You do not need to spend more time in real estate than your 9-to-5.

This is why it’s called a loophole. The barrier is way lower.

Material Participation — What That Means for STRs

To unlock the STR loophole, you need to materially participate in your short-term rental activity. The IRS gives a few different tests, but here are the most common ones people use:

1. 500-Hour Test:

You spend at least 500 hours during the year working on the property.

2. Substantially All Test:

You did basically everything — guests, bookings, cleaning, messages, maintenance, etc.

3. 100-Hour + Most Test:

You spent at least 100 hours AND no one else (including cleaners or co-hosts) spent more time than you.

If you meet any one of those, and your average guest stay is under 7 days, you’re in business.

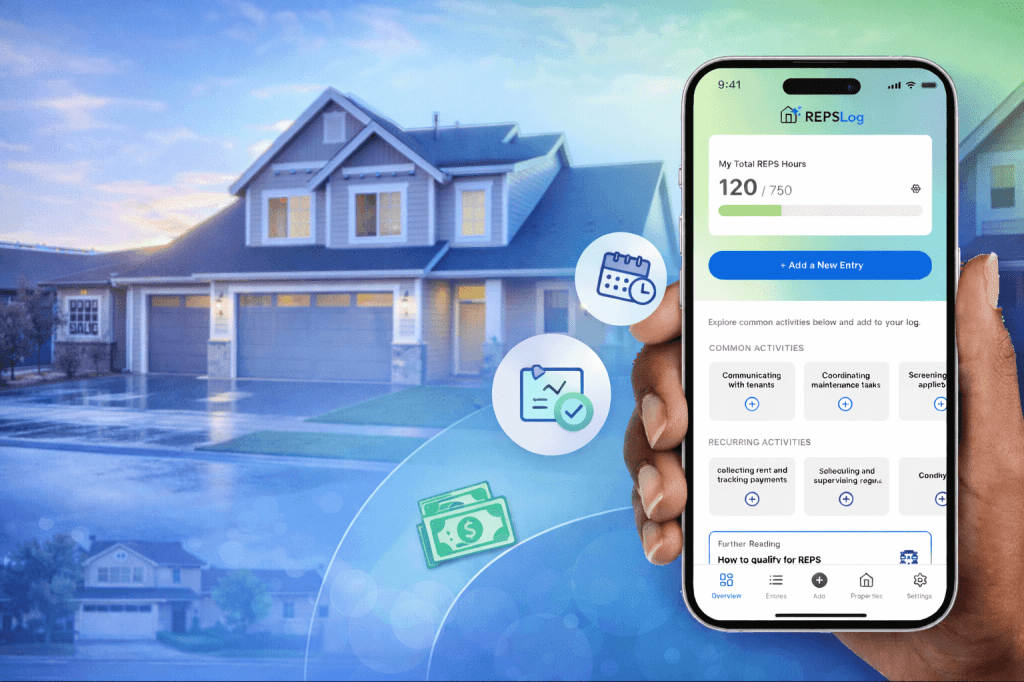

Pro tip: Keeping track of your hours can get messy fast — especially if you’re juggling multiple tasks. A simple tool like REPSLog can make it easier to log your time consistently and stay organized throughout the year.

STR Loophole in Action: A Quick Example

Let’s say you bought a short-term rental this year and did a cost segregation study that created $70,000 in bonus depreciation.

You also have a W-2 job making $130,000.

If you qualify for the STR loophole:

That $70K loss can offset your W-2 income — so now you’re only taxed on $60K.

Depending on your tax bracket, that could mean $15,000–$20,000+ in savings.

Does Airbnb Count?

Yes — Airbnb, Vrbo, and any other short-term rental platform counts as long as the average stay is 7 days or less.

If your stays are longer (say, 10-15 days), there’s still a loophole path — but you’ll need to keep your personal services (like cleaning and communication) very limited. There’s nuance here, but the 7-day rule is the clearest route.

Common Mistakes to Avoid

- Not tracking your time: Just like REPS, you need proof of material participation. I use REPSLog to quickly log what I did and when — way easier than trying to recreate my calendar at tax time.

- Letting a property manager run the show: If you’re not doing the work, you don’t qualify.

- Mixing STRs with long-term rentals: They’re treated differently — keep things clean.

- Assuming one weekend of bookings qualifies: You need consistent activity, not just a few guest stays.

- Skipping cost segregation because it sounds “too advanced”: STRs + bonus depreciation = huge unlock if you qualify.

Final Thoughts

The STR loophole isn’t shady. It’s not a trick. It’s literally in the IRS playbook — most investors just don’t know about it (or assume it’s too complicated to use).

If you’re self-managing a short-term rental — booking guests, messaging them, coordinating cleanings, and maybe doing a little cost seg magic — this is something you need to look into.

It’s one of the rare cases where you can keep your full-time job and still unlock massive tax savings from real estate.

TL;DR — STR Loophole Quick Checklist ✅

- Average guest stay is 7 days or less

- You materially participate (meet one of the tests)

- You self-manage or do most of the work yourself

- You’re tracking time and activity

- You claim losses against active income like W-2 or business profits

Boom. Tax code unlocked.

Please Note: REPSLog is NOT a lawyer or CPA, and this is not legal or financial advice. Please consult a qualified professional for guidance regarding IRS rules and regulations.