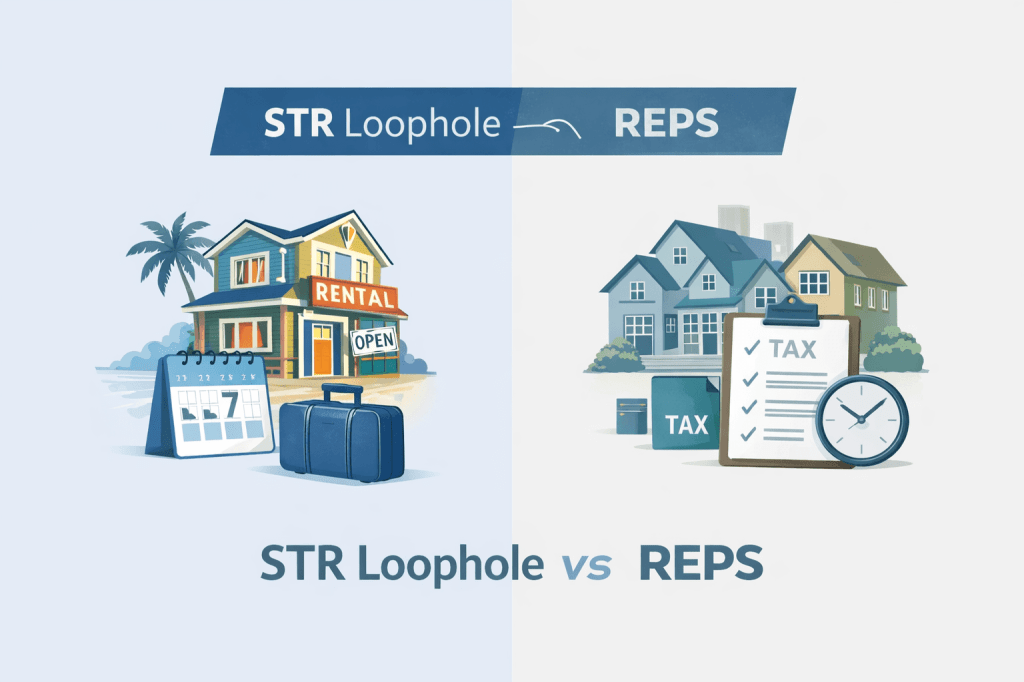

Real estate investors often hear about two powerful tax strategies: the STR loophole and Real Estate Professional Status (REPS).

They’re frequently discussed together — and often confused.

While both strategies can unlock real estate losses that would otherwise be passive, they are fundamentally different in structure, eligibility, and who they are designed for. Choosing the wrong one — or mixing them incorrectly — is a common source of audit issues.

This article explains how the strategies differ, who each one is best suited for, and why STR planning is often realistic for W-2 earners while REPS is not.

The Core Difference: Activity-Level vs Taxpayer-Level

The most important distinction is how the IRS evaluates each strategy.

- STR Loophole → An activity-level strategy

- REPS → A taxpayer-level status

This distinction is rooted in the passive activity rules outlined by the Internal Revenue Service in Publication 925.

It affects how hours are counted, how losses are unlocked, and how difficult each strategy is to qualify for.

What the STR Loophole Is (and Who It’s For)

The STR loophole applies to short-term rentals, generally defined as properties with an average stay of 7 days or less (or 30 days with substantial services).

Short-term rentals are treated differently under the tax code. They are not automatically considered rental activities, which means they can generate non-passive income or losses if the taxpayer materially participates.

Material participation is tested under IRS rules and described in IRS Publication 925. Common tests include:

- 500+ hours of participation

- Participation exceeding that of any other individual

- Substantially all participation

Who the STR Loophole Is Best For

The STR loophole is often ideal for:

- High-income W-2 earners

- Business owners with limited schedule flexibility

- Investors with one or a few hands-on STRs

- Anyone unable to shift most of their working time to real estate

Most importantly: REPS is not required to use this strategy.

What REPS Is (and Who It’s For)

Real Estate Professional Status is a designation applied to the taxpayer, not to a property or activity.

To qualify, the IRS requires both:

- More than 50% of total working time in real property trades or businesses

- At least 750 hours per year in those activities

These requirements are detailed in IRS Publication 925 and repeatedly upheld in U.S. Tax Court cases such as Bailey v. Commissioner.

If you qualify for REPS and materially participate in your rental activities, long-term rental losses that would normally be passive can become non-passive, allowing them to offset other income.

Who REPS Is Best For

REPS is generally suited for:

- Full-time real estate investors

- Stay-at-home spouses managing rentals

- Investors with large long-term rental portfolios

- Those actively involved in acquisitions, rehabs, or development

REPS is a powerful strategy — but it is also much harder to qualify for.

Why REPS Is Often Not Possible With a W-2 Job

This is one of the most important practical differences between the two strategies.

To qualify for REPS, more than 50% of your total working time must be in real estate. For most W-2 employees, this creates a mathematical problem:

- A full-time W-2 job typically requires ~2,000 hours per year

- To pass the 50% test, you would need more than 2,000 hours in real estate

- On top of that, you must still meet the 750-hour minimum

For most W-2 earners, this is not realistic, and claiming REPS in that situation is a common audit trigger.

By contrast, the STR loophole does not require any comparison to your W-2 time.

You only need to materially participate in the STR activity — which is why STR planning is often viable for high-income W-2 professionals while REPS is not.

Why STR Hours Usually Don’t Count Toward REPS

Even when STRs are grouped, STR work is generally treated as separate from long-term rental activities used for REPS qualification.

That means:

- STR hours may unlock STR losses

- STR hours usually do not help you reach REPS qualification

- Grouping STRs does not change your taxpayer status

This distinction is emphasized by tax professionals and reflected in IRS guidance and court rulings.

Using Both Strategies in the Same Year

It is possible to use both strategies — but they must be documented separately.

An investor may:

- Use the STR loophole to offset income with STR losses

- Independently qualify (or not qualify) for REPS based on long-term rental work

What you cannot do is assume the hours or losses automatically merge.

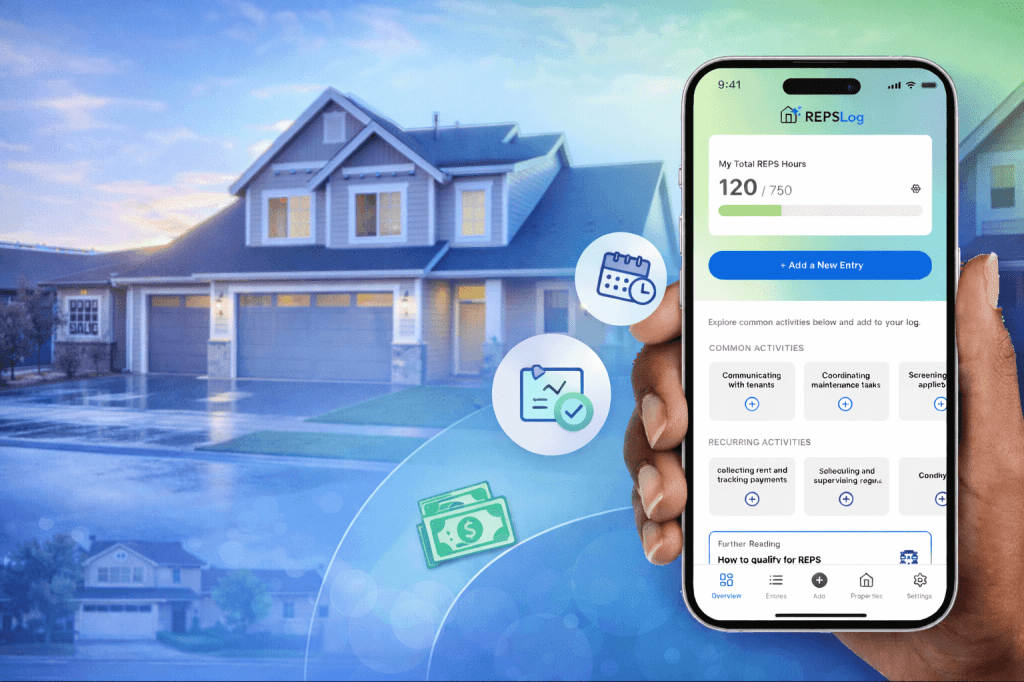

How REPSLog Helps Investors Stay Compliant

Many investors don’t fail because they chose the wrong strategy — they fail because they documented it incorrectly.

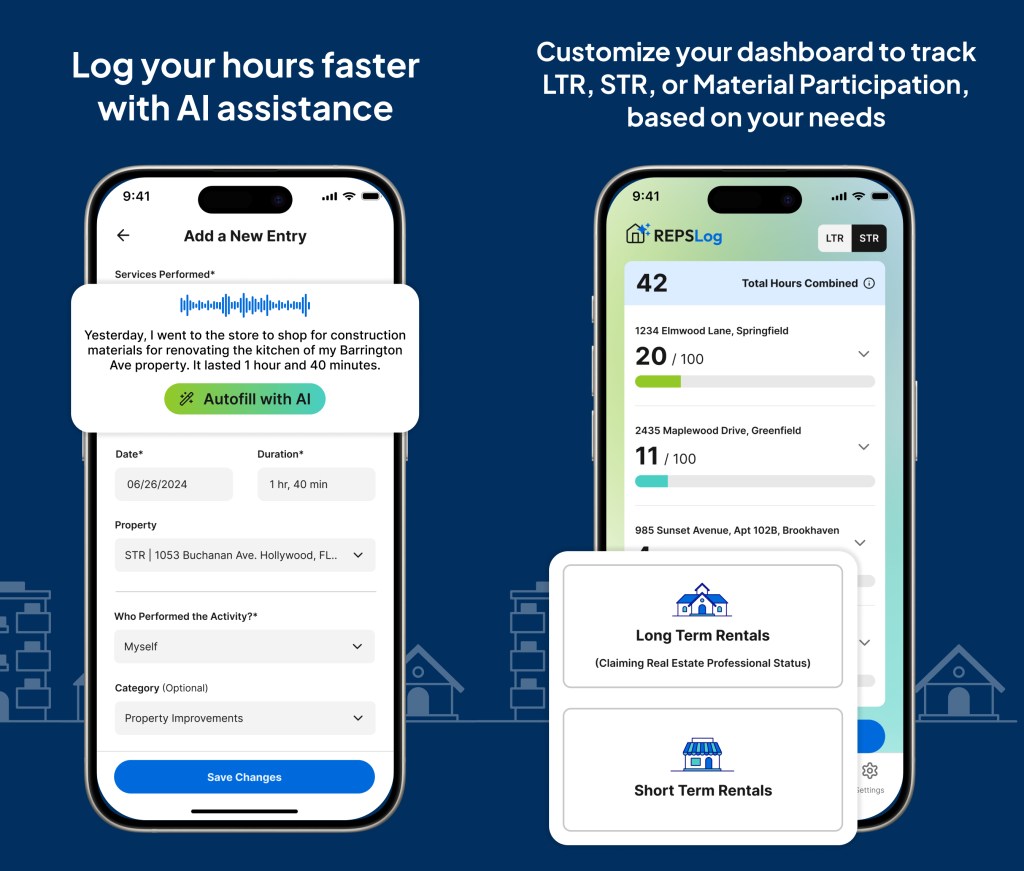

The REPSLog App helps investors:

- Track hours by property and activity

- Keep STR and long-term rental work clearly separated

- Maintain contemporaneous records, which the IRS consistently favors

- Export structured logs that CPAs can review and defend

This is especially important for investors using both STR and REPS strategies in the same tax year.

Final Thoughts

The STR loophole and REPS are not interchangeable — and they are not designed for the same investors.

- STR planning is often realistic for W-2 earners

- REPS is typically reserved for those whose primary occupation is real estate

- Grouping STRs can help with material participation, but it does not change taxpayer status

Understanding these differences upfront leads to better planning — and far fewer surprises during tax season or an audit.

Please Note: REPSLog is NOT a lawyer or CPA, and this is not legal or financial advice. Please consult a qualified professional for guidance regarding IRS rules and regulations.