Real Estate Professional Status (REPS) is one of the most powerful tax strategies available to real estate investors — and one of the most misunderstood when it comes to married couples.

A question that comes up constantly is:

“If only one spouse qualifies for REPS, do both spouses benefit?”

The answer is yes — but only if the rules are followed carefully.

Understanding how the IRS evaluates hours, participation, and joint returns is key to using REPS correctly without creating audit risk.

This guide explains how REPS works for married couples, when a spouse’s hours actually matter, and why grouping properties changes the math.

How REPS Works on a Joint Tax Return

REPS is an individual status, not a household designation.

However, when a married couple files jointly:

- Only one spouse needs to qualify for REPS.

- If that spouse qualifies and materially participates in the rental activities, losses may become non-passive.

- Those losses can offset income across the entire joint return.

The IRS framework for passive activity losses and real estate professional rules is outlined in Internal Revenue Service Publication 925, which distinguishes between individual qualification and activity-level participation.

The Two Gates Every Married REPS Strategy Must Pass

A helpful way to understand how hours work is to think in terms of two separate gates.

Gate 1 — Qualifying as a Real Estate Professional

One spouse must independently meet:

- 750+ hours in real property trades or businesses

- More than 50% of their total working time in real estate

Spouse hours cannot be combined here.

Even if both spouses work on rentals, only one person’s hours determine REPS qualification.

This is why REPS is often difficult for households where both spouses have full-time W-2 jobs. If someone works 2,000 hours annually in a W-2 role, they would typically need to exceed that amount in real estate hours to pass the 50% test — something that is rarely practical.

Gate 2 — Material Participation in the Rental Activities

After REPS is achieved, the IRS asks a second question:

Are the rental activities themselves active or passive?

This is where spouse involvement can make sense.

Under IRS rules, spouses filing jointly may combine their participation when determining material participation in an activity. That means both spouses’ efforts can help demonstrate that the rentals are actively operated — even though only one spouse qualified for REPS.

In practice:

- The qualifying spouse still needs 750+ hours personally.

- The other spouse’s work supports how active the rental operations appear.

When a Spouse’s Hours Actually Help

Many investors assume spouse hours help reach REPS qualification. They don’t.

Instead, spouse hours can be helpful in situations like:

- Supporting material participation across properties

- Showing consistent operational involvement

- Strengthening documentation during CPA review or audit

For example:

- Spouse A qualifies for REPS with 820 hours.

- Spouse B contributes 200 hours assisting with leasing, tenant communication, or admin tasks.

Those 200 hours don’t help Spouse A reach 750 — but they help demonstrate that the rental activity itself is actively managed.

Grouping Changes How Much Spouse Hours Matter

One of the biggest strategic decisions in REPS planning is whether rental properties are grouped.

Grouping allows multiple rentals to be treated as one activity for material participation purposes.

If Properties Are NOT Grouped

Material participation is tested per property.

This means:

- Each rental must show enough activity individually.

- Spouse hours may play a bigger role in reaching participation thresholds across multiple properties.

Households that don’t group often rely more heavily on combined effort.

If Properties ARE Grouped

Material participation is tested across the entire portfolio.

In many grouped scenarios:

- The REPS spouse’s own hours are often enough to meet participation requirements.

- Spouse hours become supportive rather than necessary from a mathematical standpoint.

Grouping doesn’t change REPS qualification — but it simplifies Gate 2 dramatically.

Why REPS Is Often Easier for Certain Married Couples

REPS tends to work best when:

- One spouse has flexible or limited outside employment.

- One spouse manages rentals as a primary role.

- The couple files jointly and wants losses to offset high income.

Common successful setups include:

- One high-income W-2 spouse + one real-estate-focused spouse

- Stay-at-home spouses managing portfolios

- Self-employed spouses transitioning into real estate

When both spouses work full-time W-2 jobs, REPS becomes much harder due to the 50% working-time requirement.

Common Misconceptions Married Investors Have

Some of the most frequent misunderstandings include:

- Thinking spouses can combine hours to reach 750

- Assuming joint ownership equals joint qualification

- Believing that spouse involvement alone creates REPS eligibility

- Not understanding how grouping changes participation in tests

In reality:

- REPS qualification is individual.

- Material participation can reflect household effort.

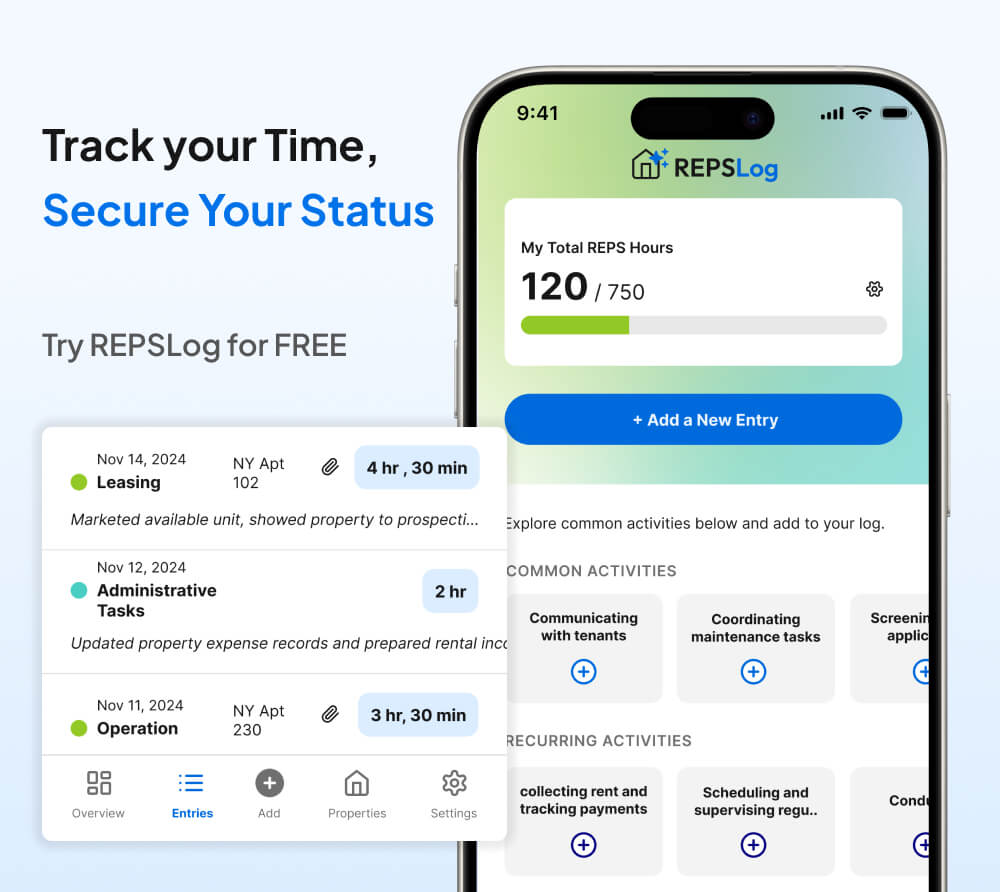

How REPSLog Helps Married Investors Stay Organized

For married couples, one of the hardest parts of REPS isn’t doing the work — it’s clearly showing who performed which activities.

REPSLog helps investors:

- Track hours separately by spouse and property

- Maintain contemporaneous records aligned with IRS expectations

- Organize activities for grouped or non-grouped portfolios

- Export clean logs that CPAs can review and defend

This clarity is especially useful when one spouse qualifies for REPS while the other contributes operational support.

FAQs

Can spouses combine hours to reach 750 hours for REPS?

No. One spouse must independently meet the 750-hour and 50% working-time tests. Hours cannot be combined for REPS qualification.

If only one spouse qualifies for REPS, do both benefit?

Yes. When filing jointly, non-passive losses may offset income across the entire return if one spouse qualifies and materially participates.

Do spouse hours matter at all?

Yes, but mainly for supporting material participation, not for becoming a real estate professional.

Do grouping properties change how spouse hours work?

Yes. Grouping allows material participation to be tested across the portfolio, which often reduces reliance on combined household hours.

Why is REPS difficult for dual W-2 households?

Because one spouse must spend more time in real estate than in any other job, a requirement outlined in Internal Revenue Service Publication 925.

Do spouses need to own the properties separately?

No. Qualification is based on participation, not ownership structure.

Please Note: REPSLog is NOT a lawyer or CPA, and this is not legal or financial advice. Please consult a qualified professional for guidance regarding IRS rules and regulations.