Qualifying as a real estate professional under IRC Section 469(c)(7) is only the first gate. To actually deduct your rental losses against active income, you must also prove that you materially participated in each rental activity — or in a single grouped rental activity if you have made a grouping election. This is where the seven material participation tests come in, and understanding them is essential for any investor building a REPS-based tax strategy.

The material participation rules live in Treasury Regulation Section 1.469-5T, and they apply to all taxpayers claiming non-passive treatment of business activities. For real estate investors, these tests determine whether your rental operations are treated as active businesses (losses deductible) or passive activities (losses suspended). Getting this right can mean the difference between a six-figure tax deduction and nothing at all.

Why Material Participation Matters for REPS

Let us set the stage with a common scenario. Sarah qualifies as a real estate professional — she meets the 750-hour test and the more-than-half test. She owns five rental properties that collectively generate $120,000 in paper losses after depreciation.

Without material participation in those properties, Sarah’s REPS status is essentially meaningless for loss deduction purposes. The properties remain passive activities, and the $120,000 in losses stays suspended. She went through the effort of qualifying as a real estate professional, but she still cannot use the losses.

Only when Sarah proves material participation does the REPS designation activate. At that point, her rental activities are reclassified from passive to non-passive, and the $120,000 in losses flows through to offset her household’s other income.

This is why understanding — and strategically selecting — the right material participation test is just as important as qualifying for REPS itself.

The Seven Tests: A Complete Breakdown

The IRS provides seven alternative tests for establishing material participation. You only need to satisfy one of them for each activity (or for your grouped rental activity). Here they are in the order they appear in the regulations, with analysis of how each one applies to real estate investors.

Test 1: The 500-Hour Test

The rule: You participated in the activity for more than 500 hours during the tax year.

How it works for real estate investors: This is the most straightforward and commonly used test. If you spend more than 500 hours working on your rental activities during the year, you have satisfied material participation. For investors who have made a grouping election, the 500 hours can be spread across all properties combined.

Practical math: 500 hours across 52 weeks equals roughly 9.6 hours per week — less than 2 hours per business day. For a hands-on investor managing multiple properties, this is very achievable. Property visits, tenant management, maintenance coordination, bookkeeping, and acquisition research add up quickly.

Why it is popular: It is simple, objective, and does not require comparison to anyone else’s hours. You either hit 500 or you do not. And since REPS already requires 750 hours in real property trades or businesses, most qualifying investors easily surpass 500 hours in their rental activity alone.

Documentation tip: The same time log you maintain for REPS qualification serves double duty here. Make sure entries are categorized by property (or note that they apply to the portfolio generally) so your log supports both the REPS claim and the material participation claim.

Test 2: The Substantially-All Test

The rule: Your participation in the activity constituted substantially all of the participation by all individuals (including non-owners) for the tax year.

How it works for real estate investors: If you are the only person doing meaningful work on your rental properties, this test is satisfied automatically. “Substantially all” is generally interpreted as 90% or more of total participation hours.

When it applies: This test is most useful for small-portfolio investors who self-manage everything. If you have two rental properties and you handle all showings, maintenance, bookkeeping, and tenant communications yourself — with no property manager, no handyman on retainer, and no partners — your participation is substantially all of the participation.

Limitations: The moment you hire a property manager, this test becomes difficult to satisfy. A professional management company might log hundreds of hours on your properties annually. Your participation would need to dwarf theirs, which is unlikely if you are paying someone to handle day-to-day operations.

Best for: Solo investors with small, self-managed portfolios.

Test 3: The 100-Hour / More-Than-Anyone-Else Test

The rule: You participated in the activity for more than 100 hours during the tax year, and no other individual participated more hours than you did.

How it works for real estate investors: This is the “I’m the most involved person” test. It has a low absolute threshold (just over 100 hours) but requires that nobody else — not a property manager, not a co-owner, not a contractor — put in more hours than you did on the activity.

When it applies: This works well when you are actively involved but have hired some help. Say you spend 150 hours per year on a rental property, and your part-time handyman spends 80 hours on repairs for that same property. You pass: more than 100 hours and more than anyone else.

Limitations: If your property manager logs 200 hours on your properties and you log 150, you fail this test — even though 150 hours is substantial involvement. The comparative element is the key constraint.

Important note for grouped activities: If you have made a grouping election, all of your properties are one activity. You need to ensure no single individual (across all your properties) logged more hours than you did. This can be tricky with active property managers.

Test 4: The Significant Participation Aggregation Test

The rule: You participated in the activity for more than 100 hours, the activity is a “significant participation activity” (SPA), and your aggregate hours across all SPAs exceed 500 hours for the year.

How it works for real estate investors: This test is designed for people who participate meaningfully in multiple activities but do not hit 500 hours in any single one. If you have three rental properties, spend 180 hours on each, and have not made a grouping election, none individually meets the 500-hour test. But combined, your 540 hours across all three SPAs satisfies this test.

When it applies: Primarily useful for investors who have not made a grouping election and own multiple properties, each receiving moderate but not dominant attention. In practice, most REPS investors make the grouping election, which makes the 500-hour test (Test 1) simpler to apply.

Key detail: Each individual activity must still meet the 100-hour threshold to qualify as a significant participation activity. A property where you logged only 60 hours cannot be included in the aggregation.

Test 5: The Prior-Year Material Participation Test

The rule: You materially participated in the activity for any 5 of the prior 10 tax years.

How it works for real estate investors: If you have a track record of material participation in a rental activity, this test provides a backward-looking qualification. The 5 years do not need to be consecutive — any 5 out of the prior 10 will suffice.

When it applies: This is a safety net for investors going through a transition year. Perhaps you had surgery, took a sabbatical, or dealt with a family emergency that reduced your hours below normal. If you materially participated in the prior 5 out of 10 years, you still qualify this year even if your current-year hours fall short of other tests.

Limitations: This test does not help first-time REPS filers or investors with newer properties. You need a multi-year history of material participation to invoke it.

Test 6: The Personal Service Activity Test

The rule: The activity is a personal service activity (health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting), and you materially participated in any 3 prior tax years.

How it works for real estate investors: It does not. This test is specifically limited to personal service activities as defined in the regulations, and real estate rental activities do not qualify. Real estate investors can effectively ignore this test.

Test 7: The Facts and Circumstances Test

The rule: Based on all the facts and circumstances, you participated in the activity on a regular, continuous, and substantial basis during the tax year.

How it works for real estate investors: This is the catch-all test, and it is also the most subjective and the most difficult to rely upon. The IRS and Tax Court will look at the totality of your involvement — how often you participated, how consistently, and how meaningful your contributions were.

Critical limitation: The regulations explicitly state that this test cannot be satisfied if you participated for 100 hours or less during the year, regardless of the nature of your participation. So even under this flexible standard, there is a floor.

When it applies: Some investors attempt this test when they fall short of the bright-line thresholds of Tests 1-5. However, relying on facts and circumstances is inherently risky because it invites subjective IRS evaluation. Tax Court outcomes under this test are unpredictable.

Best practice: Treat this test as a last resort, not a strategy. If you are structuring your activities around a facts-and-circumstances argument, you are building on sand.

Which Tests Matter Most for Real Estate Investors?

For the majority of REPS-qualifying investors, the decision tree is simple:

- Make the grouping election (treat all rentals as one activity)

- Use Test 1 (500 hours) to prove material participation across the grouped activity

- Maintain a detailed time log that supports both REPS qualification and material participation

If you have not made a grouping election — perhaps because you have a mix of profitable and loss-generating properties and want to keep them separate for strategic reasons — then you will need to satisfy material participation for each property individually. In that case, Tests 1, 2, and 3 become your primary tools.

For properties where you are deeply involved, Test 1 (500 hours) per property works if you have a small, concentrated portfolio.

For properties where you are the sole operator, Test 2 (substantially all) may apply without needing to count hours at all (though you should still track them).

For properties with moderate involvement, Test 3 (100 hours, more than anyone else) provides a lower threshold if you can confirm no one else is logging more hours on that property.

How Spouses Factor Into Material Participation

This is one of the most important — and most frequently confused — aspects of REPS and material participation.

The Combining Rule for Material Participation

For purposes of material participation, a married couple filing jointly can combine their hours on a given activity. If one spouse logs 300 hours on the rental portfolio and the other logs 250 hours, their combined 550 hours satisfies Test 1 (500 hours).

This is explicitly permitted under Treasury Regulation Section 1.469-5T(f)(3), which states that the participation of a taxpayer’s spouse is treated as the participation of the taxpayer.

The Non-Combining Rule for REPS Qualification

Here is where confusion arises. While spouses can combine hours for material participation, they cannot combine hours for the REPS 750-hour and more-than-half tests. One spouse must individually meet both REPS requirements.

Example that works: Alex qualifies as a real estate professional (800 hours in real estate, part-time job with 600 non-real-estate hours). Alex’s spouse Jordan logs 200 hours helping with property management. For material participation on their grouped rental activity, Alex and Jordan combine their hours: 800 + 200 = 1,000 hours, easily satisfying the 500-hour test. Alex’s individual REPS qualification unlocks the deduction for both of them on their joint return.

Example that fails: Neither Alex (500 hours in real estate, 900 hours at W-2 job) nor Jordan (400 hours in real estate, 1,200 hours at W-2 job) individually qualifies as a real estate professional. Even though their combined real estate hours total 900, neither spouse passes both the 750-hour test and the more-than-half test individually. REPS is not available, regardless of their combined material participation hours.

Why This Distinction Matters

The spouse combining rule for material participation is a significant planning opportunity. It means the non-qualifying spouse’s contributions are not wasted — they count toward proving the level of involvement required for loss deductions. But the REPS qualification itself must rest on one spouse’s shoulders alone.

The STR Loophole and Material Participation

Short-term rental (STR) investors have a unique relationship with material participation because of how the IRS classifies their activity.

When the average rental period is 7 days or less, the activity is not treated as a rental activity under Treasury Regulation Section 1.469-1T(e)(3)(ii)(A). Instead, it is treated as a regular trade or business. This means STR losses can offset active income without REPS qualification — but only if the taxpayer materially participates in the STR activity.

For STR investors, material participation is not a secondary requirement layered on top of REPS. It is the primary requirement. And the same seven tests apply.

The most commonly used tests for STR material participation are:

- Test 1 (500 hours): The cleanest path. Spend more than 500 hours on your STR operations — guest communications, turnover management, pricing optimization, maintenance, marketing, and so on.

- Test 3 (100 hours, more than anyone else): Works if you are more involved than your cleaning crew, co-host, or property manager, and you log more than 100 hours. This is viable for investors who self-manage one or two STR properties.

For investors who own both long-term rentals (requiring REPS) and short-term rentals (using the STR loophole), tracking hours accurately for each activity becomes even more important, as the qualification paths are different.

Frequently Asked Questions

Can I use different tests for different properties?

Yes. If you have not made a grouping election, each property is a separate activity, and you can apply a different material participation test to each one. Property A might qualify under Test 1 (500 hours), while Property B qualifies under Test 3 (100 hours and more than anyone else).

Does the grouping election lock me in forever?

Generally, yes. Once you make a Section 469 grouping election, it applies for the current year and all subsequent years unless there is a material change in facts and circumstances. Consult your CPA before making this election, as it has long-term implications.

What if I hire a property manager — can I still materially participate?

Absolutely. Hiring a property manager does not disqualify you from material participation. However, it does affect which tests you can use. Test 2 (substantially all) becomes very difficult, and Test 3 (100 hours, more than anyone else) requires that your hours exceed the property manager’s. Test 1 (500 hours) remains available regardless of whether you have a property manager.

Do hours spent on a cost segregation study count?

Time you spend working with cost segregation engineers — providing property information, reviewing reports, making decisions about classifications — can count as management or operational time. However, the engineer’s hours do not count toward your material participation.

Can I retroactively make a grouping election?

The grouping election is made by attaching a statement to your tax return for the year. If you filed without the election and later wish you had made it, you would generally need to amend your return. Consult a tax professional about the feasibility and implications of a retroactive election.

How does material participation apply to real estate syndications?

Most passive investors in syndications hold limited partnership interests or are simply passive members of an LLC. They do not materially participate and cannot use their share of syndication losses to offset active income, even if they qualify as real estate professionals. Material participation requires hands-on, operational involvement in the activity.

Key Takeaways

- Material participation is required in addition to REPS qualification — without it, REPS alone does not unlock loss deductions

- You only need to pass one of the seven tests for each activity or for your grouped rental activity

- Test 1 (500 hours) is the workhorse for most REPS investors, especially those with a grouping election

- Spouses can combine hours for material participation but not for REPS qualification — a critical distinction

- The grouping election simplifies compliance by treating all rentals as one activity for material participation purposes

- STR investors use material participation as their primary qualification under the 7-day rule, independent of REPS

- Test 7 (facts and circumstances) should be a last resort, not a deliberate strategy

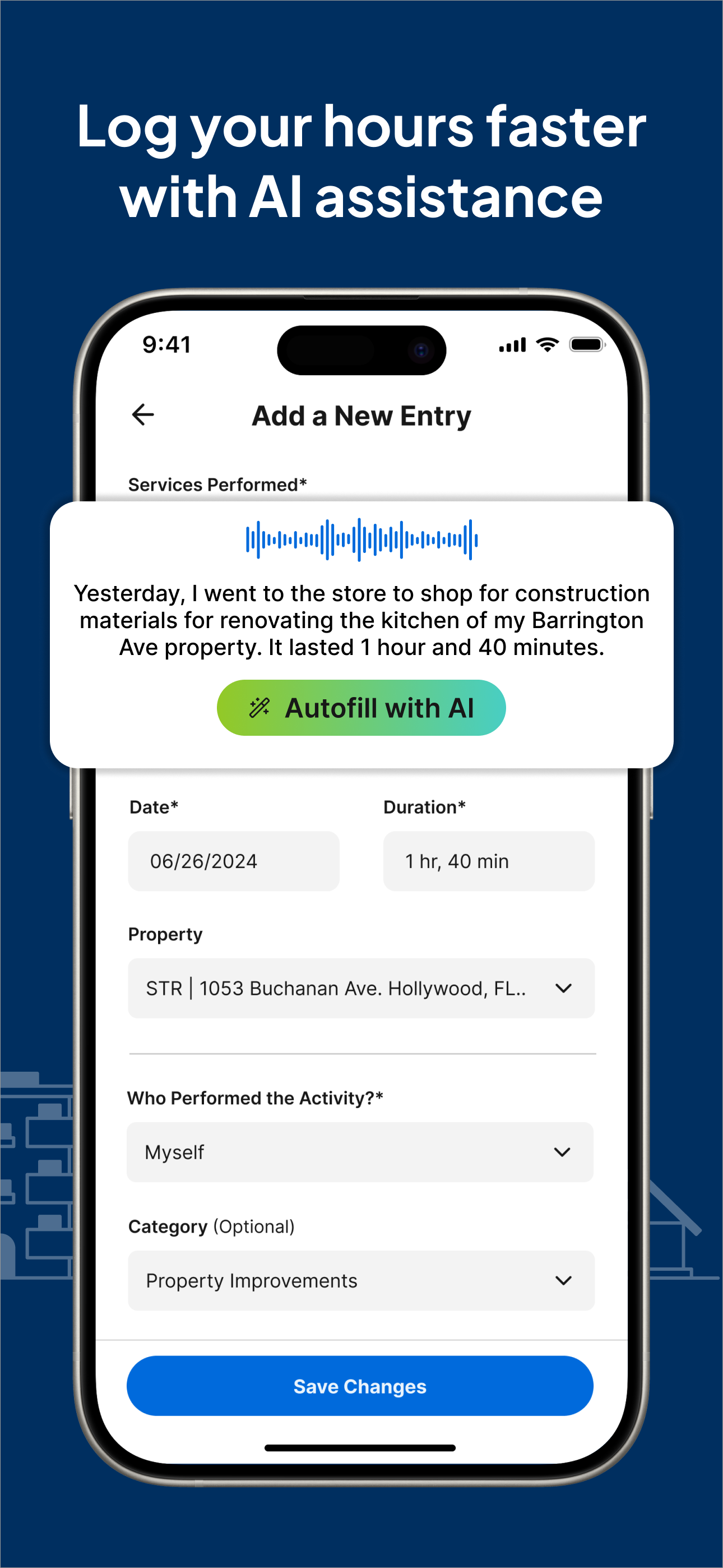

Track Material Participation With REPSLog

Proving material participation means tracking your hours with enough detail to withstand IRS scrutiny. You need precise durations, specific descriptions, property assignments, and consistency throughout the year.

REPSLog handles all of this. Log your activities in seconds with property-level categorization, and let the app calculate your running totals against the material participation thresholds. Whether you are tracking 500 hours across a grouped portfolio or 100+ hours on individual properties, REPSLog gives you real-time visibility and audit-ready exports.

Available on iOS and Android, or on the web at app.reps-log.com. Start tracking your hours free →. REPSLog is purpose-built for real estate investors who need to prove both REPS qualification and material participation. Stop guessing whether you have met the threshold — know for certain.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance specific to your situation.