Of all the strategies real estate investors use to reduce their tax burden, the REPS spouse strategy may be the most impactful per hour of effort. The basic premise: on a joint tax return, only one spouse needs to qualify as a real estate professional for the entire household to benefit from non-passive rental loss deductions. When executed correctly, this single qualification can shelter hundreds of thousands of dollars in household income from taxation.

This strategy is particularly powerful for households where one spouse earns a high W-2 income and the other has the flexibility to dedicate significant time to real estate activities. It is also the most commonly audited REPS configuration, which makes understanding the rules, documenting properly, and avoiding common pitfalls absolutely critical.

How the Spouse Strategy Works: The Fundamental Mechanics

The REPS spouse strategy rests on a specific provision in the tax code. Under IRC Section 469(c)(7), when a married couple files jointly, the real estate professional determination is made on a per-taxpayer basis — but the benefits flow to the joint return.

Here is what that means in practice:

- One spouse qualifies as a real estate professional by individually meeting both the 750-hour test and the more-than-half test

- The qualifying spouse’s REPS status applies to the joint return, allowing rental activities to be treated as non-passive

- Both spouses’ rental losses flow through to offset the household’s combined income — including the non-qualifying spouse’s W-2 earnings, business income, capital gains, and other active income

- For material participation, both spouses’ hours on rental activities can be combined

The result is that a household earning $500,000 in W-2 income with $200,000 in rental losses (driven by depreciation and cost segregation) could potentially reduce taxable income to $300,000 — a tax savings that can exceed $70,000 in a single year at the top federal brackets.

Who This Strategy Is Designed For

The REPS spouse strategy works best when the household has a clear division: one spouse generates high active income, and the other has the time and involvement to qualify as a real estate professional.

The Stay-at-Home Parent

This is the most common and often the most straightforward REPS spouse profile. A parent who is not employed outside the home has zero non-real-estate professional hours, which means the more-than-half test is satisfied with any amount of qualifying real estate work. They only need to clear the 750-hour absolute threshold.

Example: Lisa stays home with two school-age children. Her spouse David earns $350,000 as a software engineer. Lisa manages the couple’s six rental properties — handling tenant communications, coordinating maintenance, managing bookkeeping, and overseeing two properties being renovated. She logs approximately 900 hours during the year on these activities.

Lisa easily qualifies:

- 750-hour test: 900 hours exceeds 750 (passed)

- More-than-half test: Lisa has zero other professional hours, so 100% of her professional time is in real estate (passed)

The couple’s rental losses (say, $160,000 after depreciation) now offset David’s $350,000 income on their joint return. Their taxable income drops to $190,000 before other deductions.

The Part-Time Worker

A spouse who works part-time in a non-real-estate field can still qualify, provided their real estate hours exceed their non-real-estate work hours.

Example: Marcus works 20 hours per week as a freelance graphic designer (approximately 1,000 hours per year). He and his wife Jennifer own eight rental properties. Marcus spends mornings managing the portfolio before starting his design work each afternoon.

For Marcus to qualify:

- 750-hour test: He needs more than 750 hours in real estate (approximately 15 hours per week)

- More-than-half test: He needs more than 1,000 hours in real estate, since he has 1,000 non-real-estate hours

Marcus needs to log at least 1,001 hours in qualifying real estate activities. That works out to about 19.3 hours per week — ambitious but achievable for someone managing eight properties, especially if some are short-term rentals or undergoing renovation.

The Retired Spouse

A retired spouse with no other employment has the same advantage as a stay-at-home parent — zero non-real-estate hours makes the more-than-half test automatic. If the other spouse continues working and earning income, the retired spouse’s REPS qualification can generate significant tax savings during the transition years when the portfolio is still heavily leveraged and generating paper losses.

The Real Estate Agent Spouse

Perhaps the easiest path to REPS qualification. A spouse who works as a licensed real estate agent or broker accumulates qualifying hours through their day job. Showing properties, managing transactions, prospecting, attending closings, completing continuing education — all of it counts toward the 750 hours and the more-than-half test.

Example: Rachel is a full-time real estate agent logging 1,800 hours per year in brokerage activities. Her husband Tom is a physician earning $450,000. Rachel qualifies as a real estate professional through her brokerage work alone, and the couple’s rental portfolio losses offset Tom’s medical practice income.

This scenario is especially powerful because Rachel does not even need to manage the rental properties to qualify as a real estate professional — her brokerage hours satisfy both tests. She does, however, still need to demonstrate material participation in the rental activities for those losses to be deductible (more on this below).

The Doctor/High-Earner Household: A Detailed Example

The REPS spouse strategy is frequently discussed in the context of physician households, but it applies equally to any high-income earner — attorneys, executives, business owners, tech professionals, and finance professionals.

Let us walk through a comprehensive example.

The household:

- Dr. James Chen: Orthopedic surgeon, W-2 income of $520,000, works 2,200 hours per year at the hospital and clinic

- Maria Chen: Manages the couple’s real estate portfolio of 12 rental units across 4 properties

Maria’s annual real estate activities:

| Activity | Monthly Hours | Annual Hours |

|---|---|---|

| Property inspections and visits | 12 | 144 |

| Tenant screening, communications, and management | 10 | 120 |

| Maintenance coordination and contractor oversight | 15 | 180 |

| Bookkeeping, financial analysis, and reporting | 8 | 96 |

| Acquisition research and due diligence | 6 | 72 |

| Lease negotiations and renewals | 4 | 48 |

| Property marketing and listings | 3 | 36 |

| Insurance and tax assessment management | 2 | 24 |

| Education and professional development | 4 | 48 |

| Travel between properties | 6 | 72 |

| Total | 70 | 840 |

Maria’s qualification analysis:

- 750-hour test: 840 hours exceeds 750 (passed)

- More-than-half test: Maria has no other professional employment, so 100% of her professional hours are in real estate (passed)

- Result: Maria qualifies as a real estate professional

Material participation (using grouping election):

- Maria’s 840 hours alone satisfy the 500-hour material participation test

- Even without a grouping election, Maria could demonstrate material participation on each of the 4 properties individually

Tax impact:

- The 12 rental units generate $85,000 in net rental income before depreciation

- After regular depreciation: net loss of $65,000

- After cost segregation and bonus depreciation on a recent acquisition: net loss of $210,000

- With REPS, the $210,000 loss offsets Dr. Chen’s $520,000 income

- Taxable income drops from $520,000 to $310,000 (before other deductions)

- Estimated federal tax savings: approximately $75,000

Without REPS, the $210,000 loss would be suspended as passive, providing zero current-year tax benefit. The Chens would pay full taxes on Dr. Chen’s $520,000 income.

The Math for Different Employment Scenarios

Understanding the hour requirements for different scenarios helps with planning:

Scenario 1: No Outside Employment

- More-than-half test: Automatic (0 non-real-estate hours)

- 750-hour test: Need 751+ real estate hours

- Weekly commitment: approximately 14.5 hours

Scenario 2: 10 Hours/Week Side Job (520 hours/year)

- More-than-half test: Need 521+ real estate hours

- 750-hour test: Need 751+ real estate hours (this is the binding constraint)

- Weekly commitment: approximately 14.5 hours in real estate

Scenario 3: 20 Hours/Week Part-Time Job (1,040 hours/year)

- More-than-half test: Need 1,041+ real estate hours (this is the binding constraint)

- 750-hour test: 1,041 automatically exceeds 750

- Weekly commitment: approximately 20 hours in real estate

Scenario 4: 30 Hours/Week Employment (1,560 hours/year)

- More-than-half test: Need 1,561+ real estate hours (this is the binding constraint)

- 750-hour test: 1,561 automatically exceeds 750

- Weekly commitment: approximately 30 hours in real estate

Scenario 5: Full-Time 40 Hours/Week Job (2,080 hours/year)

- More-than-half test: Need 2,081+ real estate hours

- This is effectively a second full-time job — extremely difficult to achieve and sustain

- This scenario rarely works unless the “full-time job” is itself in real estate

The takeaway is clear: the more non-real-estate employment hours the qualifying spouse has, the harder it becomes to satisfy the more-than-half test. This is why the strategy works best when the qualifying spouse has minimal or no outside employment.

Combining Hours for Material Participation: The Crucial Distinction

One of the most important and frequently misunderstood aspects of the REPS spouse strategy is where spouses can and cannot combine hours.

Where You CANNOT Combine Hours

REPS qualification. Each spouse is evaluated independently. If neither spouse individually meets both the 750-hour test and the more-than-half test, the couple does not qualify for REPS. Period.

This means:

- Spouse A: 600 hours in real estate, 400 hours other work

- Spouse B: 500 hours in real estate, 1,800 hours other work

- Combined real estate hours: 1,100 — irrelevant

- Neither spouse individually meets both tests

- REPS qualification: FAILED

Where You CAN Combine Hours

Material participation. Once one spouse qualifies as a real estate professional, both spouses’ hours on the rental activity count toward material participation under Treasury Regulation Section 1.469-5T(f)(3).

This matters in two common situations:

Situation 1: The qualifying spouse’s hours alone are enough. If the qualifying spouse logs 840 hours on the rental portfolio (as in the Maria Chen example above), material participation via the 500-hour test is satisfied without needing to count the other spouse’s hours. The combination rule is a bonus but not necessary.

Situation 2: The qualifying spouse needs the other spouse’s hours to reach the threshold. This arises when the qualifying spouse spends significant time on non-rental real estate activities (brokerage, development, etc.) that count toward REPS qualification but not toward material participation in the rental activity specifically.

Example: Rachel the real estate agent logs 1,800 hours in brokerage activities and 300 hours managing the couple’s rental properties. Her husband Tom, the physician, spends 250 hours on weekends helping with property maintenance and tenant issues.

- Rachel’s REPS qualification: 2,100 total real estate hours, 0 non-real-estate hours — qualified

- Material participation on rentals: Rachel has 300 hours, Tom has 250 hours. Combined: 550 hours. The 500-hour test is satisfied using combined spousal hours.

Without the combining rule, Rachel’s 300 hours alone would not satisfy the 500-hour test, and she would need to rely on Test 3 (100 hours, more than anyone else) or Test 7 (facts and circumstances) — both of which are less certain.

Documentation Requirements for Both Spouses

When the IRS examines a REPS spouse claim, they scrutinize both spouses’ activities, not just the qualifying spouse. Proper documentation for both partners is essential.

What the Qualifying Spouse Must Document

The qualifying spouse bears the heaviest documentation burden:

A comprehensive activity log showing dates, descriptions, durations, and property associations for all real estate activities. This log must support both the 750-hour test and the more-than-half test.

Non-real-estate hours must also be trackable. If the qualifying spouse has any other employment, the IRS may ask for evidence of those hours to verify the more-than-half test. Pay stubs, employment contracts, and schedules should be retained.

A grouping election statement (if applicable) attached to the tax return, declaring that all rental properties are treated as a single activity.

What the Non-Qualifying Spouse Should Document

Even though the non-qualifying spouse does not need to meet the REPS tests, their hours matter for material participation. They should maintain:

An activity log of their real estate contributions. This does not need to be as detailed as the qualifying spouse’s log, but it should include dates, descriptions, and durations. If the couple is relying on combined hours for material participation, these records are essential.

Evidence of their primary employment hours. This serves two purposes: it confirms that the non-qualifying spouse’s professional hours are not in real estate (which would be relevant if the IRS questions why this spouse is not the one claiming REPS), and it provides context for the household’s overall time allocation.

Records Both Spouses Should Maintain

- Property purchase documents and closing statements

- Mortgage and financing records

- Insurance policies and claims

- Contractor invoices and repair receipts

- Tenant leases and communications

- Property management agreements (if applicable)

- Cost segregation studies

- Tax returns with REPS election statements

- Mileage logs for property-related travel

Common Mistakes in the Spouse Strategy

Mistake 1: Assuming a Busy Spouse Automatically Qualifies

Having a lot of properties does not equal a lot of documented hours. The qualifying spouse must actively track and document their time. “I was busy with real estate all year” is not a defense in an audit. Specific, contemporaneous logs are required.

Mistake 2: The Qualifying Spouse Takes a Job Mid-Year

Life changes happen. But if the qualifying spouse accepts part-time or full-time employment during the year, the more-than-half test recalculates. A spouse who was comfortably qualifying through September might fail for the full year if they take a job in October that adds 500 non-real-estate hours.

Planning tip: If the qualifying spouse is considering employment, run the numbers first. Calculate the real estate hours needed to maintain qualification and assess whether it is realistic alongside the new job.

Mistake 3: Not Making the Grouping Election

Without a grouping election, material participation must be proven for each property separately. For a couple with 10 properties, that means 10 separate analyses. The grouping election collapses this into one — and since combined spousal hours apply across the grouped activity, it is usually much simpler to demonstrate material participation.

Mistake 4: Claiming REPS Without Genuine Involvement

The REPS spouse strategy only works when the qualifying spouse is genuinely, substantively involved in real estate activities. If the qualifying spouse’s “involvement” consists of occasionally reviewing statements or making a few phone calls per month, the claim will not survive an audit. The IRS looks for regular, continuous, and substantial involvement.

Mistake 5: Failing to Adjust When Children Enter School

A stay-at-home parent who qualifies for REPS while children are young may find their situation changes when children enter full-day school. Suddenly, the IRS may question why a spouse with school-age children is not employed — and whether they truly spent 750+ hours on real estate. This is not a legal barrier, but it invites scrutiny. Strong documentation becomes even more important during these transition periods.

Frequently Asked Questions

Can both spouses qualify as real estate professionals?

Yes, but typically only one needs to qualify for the tax benefits to apply to the joint return. Both qualifying would provide redundancy but no additional tax benefit.

What if we file separately — can each spouse claim REPS?

Each spouse’s REPS status is determined independently regardless of filing status. However, filing separately introduces other limitations and is rarely optimal for most couples. Consult your CPA about your specific situation.

Does volunteer work count as non-real-estate hours for the more-than-half test?

Generally, no. The more-than-half test compares hours in real property trades or businesses against hours in all other trades or businesses. Volunteer work, household management, and personal activities are not “trades or businesses” and do not count on either side of the equation. This actually helps the qualifying spouse — only paid professional work outside real estate counts against them.

Can the qualifying spouse change from year to year?

Yes. REPS is an annual determination. If Spouse A qualified last year but Spouse B is better positioned this year, Spouse B can be the qualifying spouse. There is no requirement for consistency, though frequent switching may invite additional IRS scrutiny.

What about community property states?

Community property laws affect income allocation between spouses but do not change the REPS qualification rules. The 750-hour and more-than-half tests still apply on an individual basis to the qualifying spouse.

We are both real estate agents. Do we need the spouse strategy?

If both spouses are real estate agents, both likely qualify as real estate professionals independently. The spouse strategy is most relevant when only one spouse can realistically qualify. However, even in dual-agent households, understanding material participation requirements for rental activities remains important.

What happens if the qualifying spouse passes away?

REPS qualification terminates with the qualifying spouse. In the year of death, the deceased spouse’s hours through the date of death can still count. For subsequent years, the surviving spouse would need to independently qualify. This is a significant estate and tax planning consideration.

Key Takeaways

- Only one spouse needs to qualify as a real estate professional on a joint return for the household to benefit

- The strategy works best when the qualifying spouse has minimal or no non-real-estate employment, making the more-than-half test easy to satisfy

- Spouses can combine hours for material participation (proving involvement in rental activities) but NOT for REPS qualification (the 750-hour and more-than-half tests)

- Stay-at-home parents, part-time workers, retired spouses, and real estate agents are the ideal candidates for the qualifying spouse role

- Both spouses should maintain documentation — the qualifying spouse for REPS and material participation, the non-qualifying spouse for their contribution to material participation

- The grouping election dramatically simplifies the process by treating all rentals as one activity for material participation purposes

- Life changes (new jobs, children entering school, retirement) require re-evaluation of the strategy each year

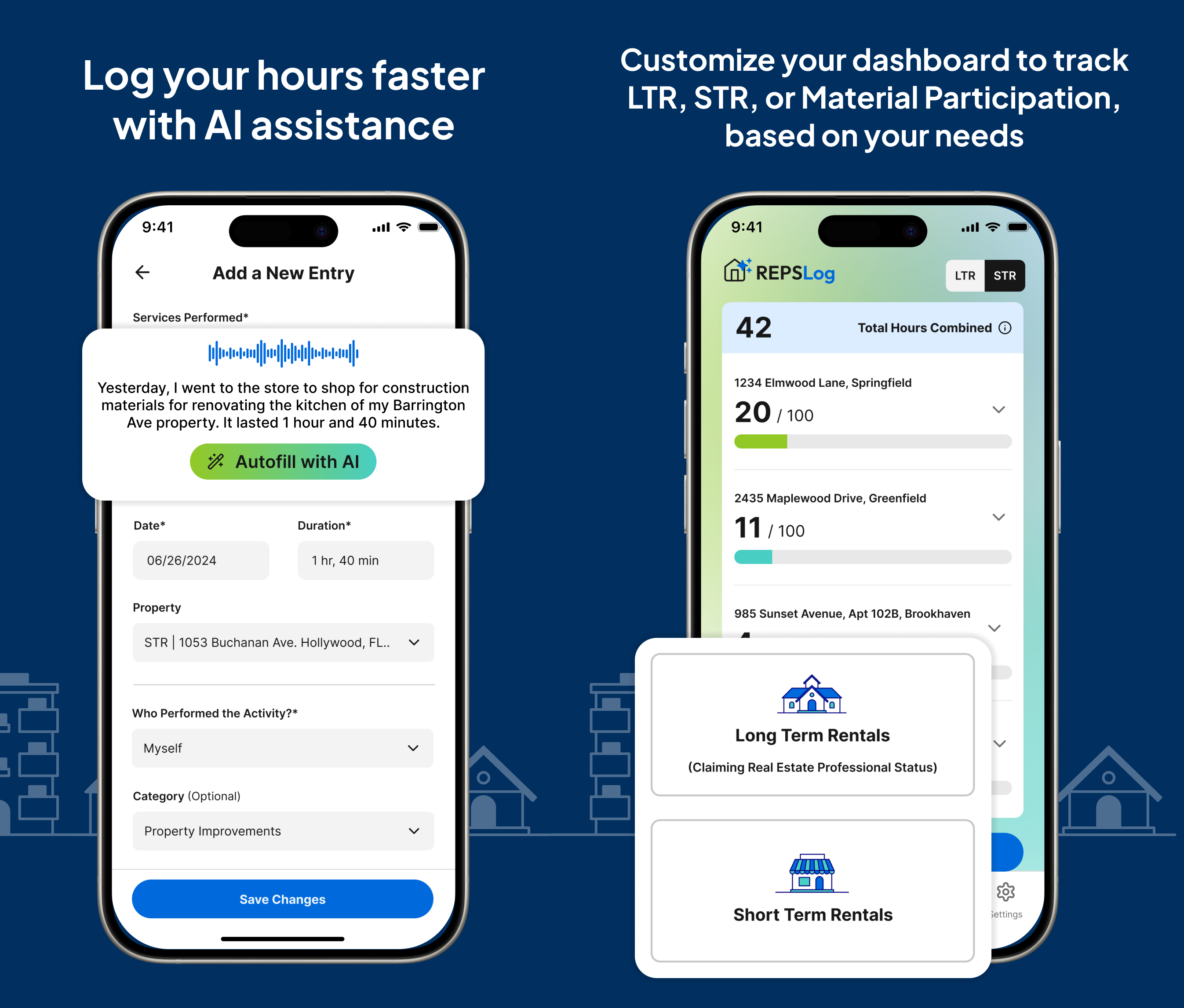

Track Both Spouses’ Hours With REPSLog

The REPS spouse strategy lives or dies on documentation. The qualifying spouse needs an airtight log of their 750+ real estate hours. The non-qualifying spouse needs records of their contributions for material participation. And both need property-level detail that can withstand IRS examination.

REPSLog makes this manageable. Each spouse can log their activities independently, with entries tied to specific properties, timestamped automatically, and categorized by activity type. The app tracks your running totals against both the 750-hour REPS threshold and the material participation benchmarks, so you always know exactly where both partners stand.

Available on iOS and Android, or on the web at app.reps-log.com. Start tracking your hours free →. REPSLog is the documentation backbone for households using the REPS spouse strategy. Protect your deductions with the same rigor you bring to your investments.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance specific to your situation.