Most REPS advice focuses on tracking your real estate hours. That makes sense because the 750-hour threshold is the headline requirement. But there is a second test that trips up taxpayers just as often, and it requires documentation of the hours you spend outside of real estate.

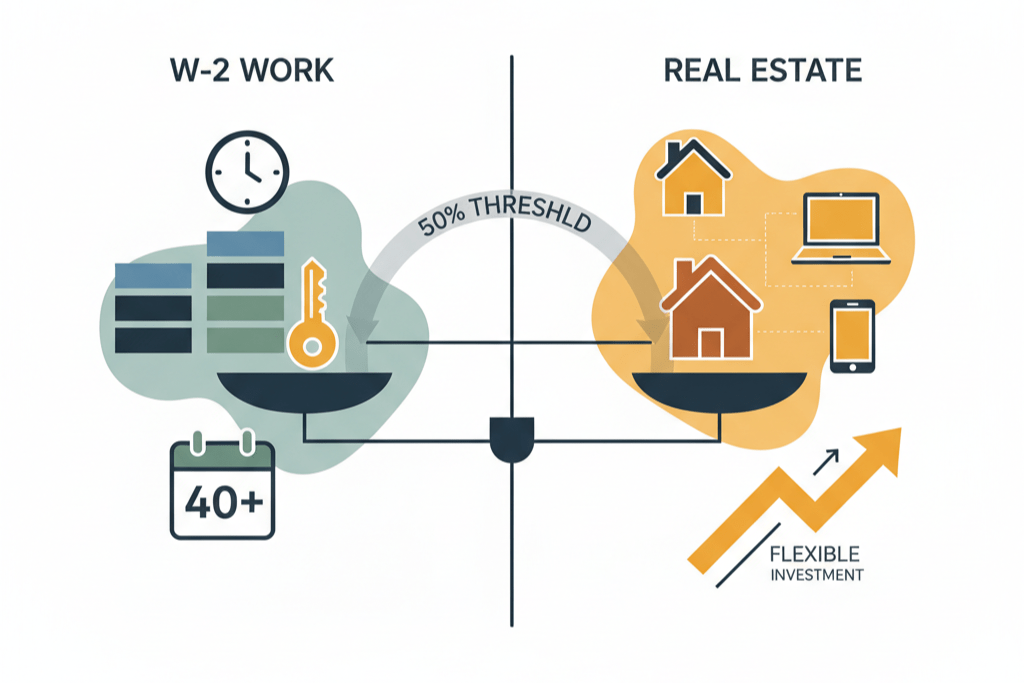

The more-than-half test under IRC Section 469(c)(7)(B) requires that your personal services in real property trades or businesses exceed half of the total personal services you perform in all trades or businesses during the tax year. In plain language: your real estate hours must be more than your non-real-estate working hours.

If you have a W-2 job, that job generates hours on the other side of the comparison. Failing to track and document those hours is a common and avoidable mistake that can undermine an otherwise strong REPS claim.

Why You Need to Track Non-Real-Estate Hours

The more-than-half test is a fraction. Your real estate hours go in the numerator. Your total hours in all trades or businesses go in the denominator. You need the numerator to be more than half the denominator.

If you track your real estate hours diligently and can show 800 hours, that looks strong. But if the IRS asks how many hours you worked at your W-2 job and you have no records, you have a problem. The IRS can calculate your W-2 hours using your wage records, and if the calculation shows 1,800 hours, your 800 real estate hours fail the more-than-half test (800 is not more than half of 2,600).

Tracking your non-real-estate hours serves two purposes. First, it gives you the data you need to evaluate whether REPS is achievable before you file your return. Second, it provides documentation to support your more-than-half claim if the IRS examines it.

How to Document W-2 Time

The quality of evidence available for your W-2 hours depends on your employment type, pay structure, and employer records. Here are the sources to leverage.

Pay stubs with hours. If your pay stubs show hours worked per pay period, these are your best evidence. They are contemporaneous, employer-generated documents that the IRS treats as reliable. Save every pay stub for the tax year, or download electronic versions from your employer’s payroll portal.

Time clock or timesheet records. If your employer uses a time clock system, electronic timesheets, or project-based time tracking, request a year-end summary of your hours. Many employers can generate this report from their payroll or HR system.

Employment contract or offer letter. Your employment agreement may specify your expected weekly hours. While this proves scheduled hours rather than actual hours, it establishes a baseline that can be adjusted for overtime, vacation, sick days, and other variations.

Annual calculation from salary. If you are a salaried employee with no hourly records, you can calculate your hours by documenting your typical work schedule. A salaried employee who works 8:30 AM to 5:00 PM, Monday through Friday, with a 30-minute lunch break, works 40 hours per week. Over 50 working weeks (accounting for two weeks of vacation), that is approximately 2,000 hours.

The IRS may accept this calculation, but it carries less weight than actual hour records. If your schedule varies, if you frequently work overtime, or if your employer contests your claimed schedule, a simple multiplication may not hold up.

Calendar and email records. Your work calendar and email timestamps can corroborate your working hours. Meeting schedules, email send times, and calendar entries showing when you were engaged in work activities all help establish your actual work pattern.

Common Mistakes in Documenting W-2 Hours

Understating actual hours. Some taxpayers report their scheduled hours rather than their actual hours in an effort to make the more-than-half test work. If you are scheduled for 35 hours per week but regularly work 45, using 35 is dishonest and dangerous. The IRS can request employer records that contradict your claimed schedule.

Ignoring overtime. Overtime hours count. If you work 40 regular hours plus 10 hours of overtime per week, your non-real-estate total is 50 hours per week, not 40. Overtime pay on your pay stubs reveals overtime hours to the IRS even if you do not report them.

Excluding commute time. Commute time to your W-2 job generally does not count as working hours for the more-than-half test. The test measures time spent performing services in a trade or business, not time traveling to and from work. This works in your favor by reducing your non-real-estate hours.

Forgetting about side businesses. The more-than-half test counts hours in all trades or businesses, not just your primary W-2 job. If you drive for a rideshare company on weekends, do freelance graphic design in the evenings, or operate any other non-real-estate business, those hours count against you. Every non-real-estate business activity adds to the denominator.

Not accounting for seasonal variation. If your work hours vary seasonally (more hours during busy season, fewer during slow periods), a simple annual average may overstate or understate your actual hours depending on when the variation falls. Track your actual hours per pay period rather than relying on averages.

What Counts as Hours in a Trade or Business

Not every hour of your day counts for the more-than-half test. The test measures hours in “trades or businesses,” which has a specific tax meaning.

Counts as W-2 hours: Time spent performing your job duties. Employer-required training. Business travel during work hours. Required meetings and conferences. Overtime. Working lunches if they are genuinely work-related.

Does not count as W-2 hours: Commuting to and from work. Personal errands during the workday. Lunch breaks (unless working through lunch). Vacation and sick days (you are not performing services). Personal phone calls and activities during work hours.

Does not count on either side: Volunteer work. Hobby activities (even if they occasionally produce income). Personal investment management (unless you are a professional trader). Household and family responsibilities.

The exclusion of non-trade-or-business activities from both sides of the fraction means the test is purely about compensated work and active business participation. This typically works in the taxpayer’s favor because it reduces the denominator more than the numerator (since real estate investors are less likely to take vacation from their real estate activities than from their W-2 job).

The Math in Practice

Here are several scenarios showing how the more-than-half test works with different W-2 schedules.

Scenario 1: Full-time W-2, 40 hours per week. W-2 hours: 40 hours x 50 weeks = 2,000. Real estate hours needed: more than 2,000 to pass the more-than-half test (since 2,000 / (2,000 + 2,000) = 50%, and you need more than 50%). This also means more than 2,000 real estate hours, which is a very high bar.

Scenario 2: Part-time W-2, 20 hours per week. W-2 hours: 20 hours x 50 weeks = 1,000. Real estate hours needed: more than 1,000. At approximately 20 hours per week of real estate work, this is achievable for active investors.

Scenario 3: Full-time W-2 with mid-year departure. W-2 hours through June: 40 hours x 26 weeks = 1,040. Real estate hours needed: more than 1,040 for the full year. If you spend 20 hours per week on real estate all year (1,000 hours) plus ramp up to 30 hours per week after leaving your job (an additional 780 hours from July through December), your real estate total of 1,780 hours easily exceeds 1,040.

Scenario 4: Variable W-2 with overtime. Base schedule: 40 hours per week. Average overtime: 8 hours per week. Actual W-2 hours: 48 hours x 50 weeks = 2,400. Real estate hours needed: more than 2,400. This is nearly impossible without full-time real estate involvement in addition to the W-2.

Strategic Considerations

Reducing W-2 hours. If the more-than-half test is your binding constraint, reducing your W-2 hours is the most direct path to qualification. Negotiating a reduced schedule, transitioning to part-time, taking unpaid leave, or leaving the position entirely all reduce the non-real-estate side of the equation. These must be genuine changes, not paper arrangements where you continue working the same hours at reduced reported time.

Timing matters. The more-than-half test is annual, so the timing of changes within the year matters. Reducing to part-time on January 1 gives you a full year of reduced hours. Reducing on July 1 gives you only six months. Plan changes for maximum calendar-year impact.

Both tests must be met simultaneously. Even if the more-than-half test is satisfied, you still need more than 750 hours of real estate activity. Meeting one test but not the other does not qualify you for REPS.

Key Takeaways

- The more-than-half test requires your real estate hours to exceed your non-real-estate working hours, making W-2 hour documentation essential.

- Pay stubs showing hours worked are your strongest evidence for W-2 time. Save every pay stub or download electronic records.

- All non-real-estate trades and businesses count, not just your primary job. Side hustles, freelance work, and gig economy activities add to your non-real-estate total.

- Do not understate your actual W-2 hours. The IRS can verify hours through employer records, pay stubs, and overtime calculations.

- Commuting, vacation days, and personal time do not count as W-2 hours for the more-than-half test. Only time performing services in a trade or business counts.

- Full-time W-2 workers at 40+ hours per week face the steepest challenge because they need more than 2,000 hours of real estate activity.

- Strategic W-2 hour reductions, if genuine, can make REPS achievable by lowering the more-than-half threshold.

Frequently Asked Questions

Does the IRS automatically know my W-2 hours?

The IRS receives your W-2 form, which shows wages but not hours. However, they can request payroll records from your employer during an audit, which may include hour data. They can also calculate estimated hours from your hourly rate and total wages, or request your employer to confirm your schedule.

What if I am a salaried employee with no hour records?

Document your typical daily schedule as accurately as possible. Note your usual start and end times, lunch breaks, and any regular variations. Corroborate with calendar entries, email timestamps, or building access records. Your employer’s HR department may also be able to confirm your standard schedule.

Do sick days and vacation days count as W-2 hours?

No. The more-than-half test counts hours of personal services performed. Days when you are not working (vacation, sick leave, holidays) do not generate hours on either side of the equation. This can work in your favor if you take significant time off from your W-2 job.

What about working from home? Does that affect hour counting?

Remote work hours count the same as in-office hours. The location where you perform your W-2 work does not affect the hour calculation. If you work from home 40 hours per week, those are 40 hours of non-real-estate activity just as they would be if you commuted to an office.

Can I use the same tracking tool for both my W-2 hours and my real estate hours?

Yes, and doing so can make the more-than-half comparison easier. Tracking both types of hours in the same system lets you see the ratio in real time throughout the year. Some investors create separate categories or projects for W-2 and real estate activities within the same tracking app.

What if my employer reduces my hours without my requesting it?

Involuntary hour reductions (furloughs, reduced schedules, layoffs) reduce your non-real-estate hours and may create an unexpected opportunity for REPS qualification. If your W-2 hours drop significantly mid-year, recalculate the more-than-half test to see if REPS becomes achievable.

Do I need to report the exact number of W-2 hours on my tax return?

Your tax return does not have a specific line for W-2 hours. However, if you claim REPS, you should be prepared to provide your W-2 hour documentation if the IRS requests it. Having the documentation ready demonstrates preparedness and strengthens your position.

Tracking your real estate hours is only half the REPS equation. You also need to understand where you stand on the more-than-half test, and that means knowing your non-real-estate hours too. REPSLog helps you track your real estate activities with the specificity the IRS requires and monitor your progress toward both REPS thresholds in real time. Get started on iOS, Android, or Web.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance tailored to your situation.