Spousal hours are one of the most misunderstood aspects of Real Estate Professional Status. Married couples who invest in real estate together frequently ask whether both spouses can qualify, whether their hours can be combined, and how filing jointly affects the REPS tests. The answers depend on which test you are discussing, because the rules treat REPS qualification and material participation very differently when it comes to spousal involvement.

This article untangles the rules, explains exactly where spousal hours help and where they do not, and addresses the common misconceptions that lead to rejected REPS claims.

The Core Rule: Only One Spouse Needs to Qualify

On a joint tax return, only one spouse needs to meet the REPS qualification requirements. If either spouse individually passes both the 750-hour test and the more-than-half test, the couple qualifies for REPS on their joint return.

This is a significant advantage for married couples. The non-qualifying spouse can work a full-time W-2 job without affecting the qualifying spouse’s REPS status. The tests are applied to each spouse individually, not to the couple collectively.

For example, if one spouse works 40 hours per week as a software engineer (approximately 2,000 hours per year) and the other spouse manages the couple’s rental properties full-time, the property-managing spouse can qualify for REPS independently. The software engineer’s 2,000 W-2 hours do not enter the property manager’s more-than-half calculation.

Hours Cannot Be Combined for REPS Qualification

This is the rule that catches most people off guard. Under IRC Section 469(c)(7), the 750-hour test and the more-than-half test are applied to each spouse individually. You cannot add your spouse’s real estate hours to yours for purposes of meeting these thresholds.

If you spend 400 hours on real estate activities and your spouse spends 400 hours, your combined 800 hours exceed 750. But neither of you individually exceeds 750. You do not qualify for REPS.

This rule exists because REPS is designed to identify individuals whose primary professional activity is real estate. Allowing hour aggregation would let two part-time participants qualify when neither one is truly a real estate professional, which would defeat the purpose of the designation.

The non-combination rule applies to both tests. Each spouse must independently accumulate more than 750 real estate hours and must independently have more real estate hours than non-real-estate hours.

Spousal Hours DO Count for Material Participation

Here is where spousal involvement becomes powerful. Under IRC Section 469(h)(5), when determining whether a taxpayer materially participates in an activity, the participation of the taxpayer’s spouse is taken into account, regardless of whether the spouse owns an interest in the activity.

This means that for the material participation test that must be met for each rental activity (or grouped rental activity), your spouse’s hours in that activity combine with yours.

Why does this matter? Because REPS qualification and material participation are separate requirements. REPS status (the 750-hour and more-than-half tests) gets you in the door. Material participation in the specific rental activity (or grouped activity) lets you deduct the losses. You need both.

Combining spousal hours for material participation can be the difference between deducting and not deducting your rental losses.

A Practical Example

Consider this scenario. Maria and David are married and file jointly. They own a portfolio of rental properties.

Maria works full-time managing the rental properties. She spends 900 hours per year on real estate activities and has no other job. She easily passes both the 750-hour test and the more-than-half test. Maria qualifies as a Real Estate Professional.

David works as an accountant 40 hours per week (approximately 2,000 hours per year). He also spends 200 hours per year helping with the rental properties, handling tenant phone calls, doing light maintenance, and reviewing financial records.

For REPS qualification: Maria qualifies individually. David does not need to qualify because only one spouse is required.

For material participation in the rental activity: Maria’s 900 hours plus David’s 200 hours gives them a combined 1,100 hours under IRC 469(h)(5). If they made a grouping election under Treas. Reg. Section 1.469-9(g), their grouped rental activity has 1,100 hours of combined participation, easily meeting the 500-hour material participation test.

Without David’s 200 hours, Maria would still meet material participation with her 900 hours. But in scenarios where the qualifying spouse’s rental-specific hours are lower (because some of their 750+ hours are in non-rental real estate activities like brokerage or development), the spouse’s hours can be the margin that makes material participation work.

When Both Spouses Want to Qualify

Can both spouses qualify for REPS simultaneously? Yes, if each one independently meets both the 750-hour test and the more-than-half test. But there is usually no tax benefit to having both spouses qualify.

REPS status on a joint return is binary: either the couple has it or they do not. Having one qualifying spouse achieves the same result as having two qualifying spouses. There is no “double REPS” benefit.

The one scenario where dual qualification might matter is if the couple is considering the possibility of filing separately in the future, divorcing, or if the qualifying spouse might lose REPS status (for example, by taking a full-time non-real-estate job). In those cases, having the second spouse independently qualified provides a backup.

Common Misconceptions

“My spouse is a real estate agent, so we qualify.” Not necessarily. Your spouse must individually meet the 750-hour test (which most full-time agents do) and the more-than-half test (which can fail if the agent has significant non-real-estate income sources). And the agent’s license alone proves nothing; the hours must be documented.

“We both work on the properties, so we can split the 750 hours.” No. Each spouse’s real estate hours are counted individually for REPS qualification. There is no splitting, sharing, or combining allowed for the 750-hour or more-than-half tests.

“My spouse does not need to track hours because I am the one qualifying.” Your qualifying spouse must track their own hours meticulously for the REPS qualification tests. Additionally, if you want to combine spousal hours for material participation under IRC 469(h)(5), the non-qualifying spouse also needs records of their participation. Undocumented hours cannot be counted.

“We can choose which spouse qualifies at tax time.” This is technically true but requires that both spouses have documented their hours throughout the year. At filing time, you can evaluate which spouse (if either) meets the tests and claim REPS through that spouse. But you cannot retroactively create documentation for a spouse who did not track.

“Spousal hours always count everywhere.” Spousal hours count for material participation (Section 469(h)(5)) but not for REPS qualification (Section 469(c)(7)). Confusing these two applications is one of the most common errors in REPS planning.

Strategies for Married Couples

Designate the qualifying spouse early. At the beginning of the tax year, determine which spouse is most likely to meet the REPS tests. That spouse should focus their time on real estate activities and minimize non-real-estate work. The other spouse can focus on W-2 employment, knowing that their real estate hours will count toward material participation but not toward REPS qualification.

Both spouses should track hours. Even though only one spouse needs to qualify, both spouses should track their real estate hours. The qualifying spouse needs the records for the REPS tests. The non-qualifying spouse needs records to support the material participation claim under IRC 469(h)(5). And if circumstances change mid-year, you want flexibility to evaluate qualification for either spouse.

Leverage the non-qualifying spouse’s real estate involvement. The non-qualifying spouse’s real estate hours do not go to waste. They count toward material participation, which is a separate and essential requirement. If the qualifying spouse’s rental-specific hours are borderline for material participation, the non-qualifying spouse’s hours can make the difference.

Consider the grouping election carefully. Under Treas. Reg. Section 1.469-9(g), the qualifying spouse can elect to treat all rental interests as a single activity. Combined spousal hours for the grouped activity are often substantial, making material participation straightforward to establish.

Plan for life changes. Job changes, health issues, children, and other life events can affect which spouse qualifies. Build flexibility into your tracking by having both spouses document their time. If the qualifying spouse takes a full-time job mid-year, the other spouse may need to step into the qualifying role, which requires their own documented hours.

Filing Status Considerations

Married filing jointly. The standard approach. One spouse qualifies for REPS, and the rental losses are deducted on the joint return against the couple’s combined income.

Married filing separately. If spouses file separately, each spouse must independently qualify for REPS on their own return if they want to claim the benefit. Rental losses on one spouse’s return can only offset that spouse’s income. Filing separately eliminates the ability to use one spouse’s REPS qualification for the other spouse’s rental activities.

Community property states. In community property states, income and deductions may be allocated differently between spouses, which can interact with REPS claims in complex ways. Consult a tax professional familiar with your state’s community property rules.

Key Takeaways

- Only one spouse needs to qualify for REPS on a joint return. The non-qualifying spouse’s W-2 hours do not affect the qualifying spouse’s tests.

- Hours cannot be combined between spouses for the 750-hour test or the more-than-half test. Each spouse must meet these thresholds independently.

- Spousal hours can be combined for material participation under IRC Section 469(h)(5). This is a separate test from REPS qualification and is essential for deducting rental losses.

- Both spouses should track their real estate hours throughout the year, even though only one needs to qualify for REPS.

- Having both spouses qualify provides no additional tax benefit on a joint return but may offer protection against future changes.

- The grouping election under Treas. Reg. Section 1.469-9(g), combined with spousal material participation hours, can make rental loss deductions significantly easier to achieve.

Frequently Asked Questions

Can my spouse’s hours save me if I am just under 750?

No. Your spouse’s real estate hours cannot be added to yours for the 750-hour test. If you have 720 hours and your spouse has 100 hours, your total for REPS qualification purposes is 720, not 820. You do not qualify.

What if my spouse and I both work on the same property at the same time?

Each spouse can count their own hours for time they work simultaneously on the same property. If both of you spend two hours painting a rental unit together, each of you logs two hours. The hours are not divided; each spouse’s participation is counted independently.

Does my spouse need to be on the property title for their hours to count?

For material participation under IRC 469(h)(5), your spouse’s participation counts regardless of whether they own an interest in the activity. The spouse does not need to be on the title, the deed, or the operating agreement. Their work on the property counts for material participation testing either way.

How do we handle REPS if we are going through a divorce?

During a divorce year, your filing status affects REPS. If you file jointly for the final time, the standard rules apply. If you file separately, each spouse needs to independently qualify for REPS on their own return. If the REPS-qualifying spouse was the one managing the properties, the other spouse loses the REPS benefit on a separate return.

Can a non-working spouse qualify for REPS?

Absolutely. A spouse who does not hold a W-2 job and spends more than 750 hours managing rental properties easily passes both tests. The 750-hour test is met through real estate hours, and the more-than-half test is met because there are no non-real-estate hours to compare against. This is one of the most common REPS qualification patterns.

What counts as spousal participation for material participation purposes?

Any real estate activity your spouse performs in connection with your rental properties counts: property maintenance, tenant communication, bookkeeping, contractor coordination, showing units, cleaning between tenants, landscaping, and any other rental management activity. The work must be genuine and documented.

Do we need separate tracking logs for each spouse?

Maintaining separate logs is advisable for clarity. Each spouse’s log shows their individual hours, which is necessary for REPS qualification testing (applied individually) and helps identify the combined total for material participation testing. Some couples prefer a single log with a column indicating which spouse performed the activity.

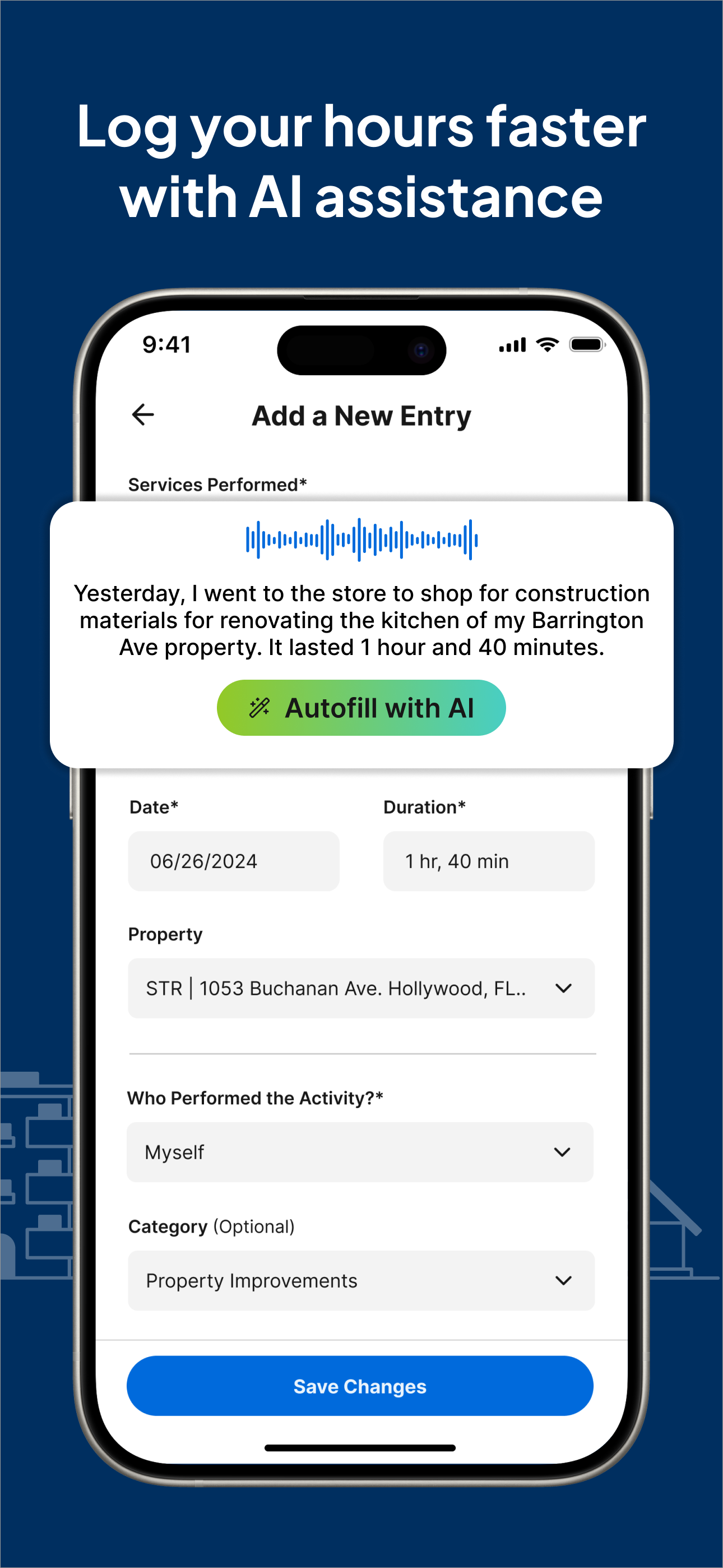

Whether one spouse or both are involved in your real estate activities, tracking every qualifying hour is what makes REPS defensible. REPSLog supports tracking by participant, making it simple to see each spouse’s hours individually for REPS qualification and combined for material participation. Track your hours on iOS, Android, or Web.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance tailored to your situation.