It is June, and you just learned about Real Estate Professional Status. You have been managing rental properties all year, but you have not been tracking a single hour. The question hits you immediately: is it too late?

The short answer is that it depends on the math, the evidence you can reconstruct, and how many months remain in the year. Starting mid-year is absolutely possible, but you need to understand the numbers, the documentation challenges, and the point at which the math simply stops working.

The Two Tests You Must Pass

Before diving into timing, let us revisit the two tests that determine REPS qualification.

The 750-hour test. You must spend more than 750 hours during the tax year performing services in real property trades or businesses in which you materially participate.

The more-than-half test. The hours you spend in real property trades or businesses must constitute more than half of the total hours you work in all trades or businesses during the year.

Both tests are annual, measured from January 1 through December 31 of the tax year. There is no prorated version for people who start tracking partway through.

The Math at Different Start Dates

Understanding when the 750-hour threshold becomes mathematically impractical helps you set realistic expectations.

Starting in January or February. You have essentially the full year. At just 15 hours per week, you accumulate over 750 hours comfortably. This is the ideal scenario, and virtually anyone performing significant real estate work full-time can qualify.

Starting in March or April. You still have nine to ten months remaining, which yields roughly 39 to 43 weeks. At 18 to 20 hours per week of real estate work, you can still clear 750 hours from this point forward. However, you also need to account for the first two to three months. If you were doing real estate work during January and February but not tracking it, reconstruction of those months becomes critical.

Starting in May or June. This is where it gets tighter. With seven to eight months remaining (roughly 30 to 35 weeks), you need approximately 22 to 25 hours per week of documented real estate activity going forward. The real challenge, though, is the January-through-April gap. Without credible evidence for those months, you need the remaining months to carry nearly the entire burden.

Starting in July. Six months left, roughly 26 weeks. You would need approximately 29 hours per week of pure real estate work for the remainder of the year, assuming zero credit for the first half. That is essentially full-time, with no vacation weeks. Possible for a full-time real estate professional, but tight.

Starting in August or September. Four to five months remaining. The math demands 37 to 47 hours per week of documented real estate activity, which is barely plausible even for someone who does nothing else. At this point, your claim depends almost entirely on reconstructing hours from earlier in the year.

Starting in October or later. With three months or less remaining, reaching 750 hours from tracking alone is mathematically impossible unless you work truly extraordinary hours. Your only path to REPS qualification is reconstruction of the preceding months.

The Reconstruction Challenge

If you start tracking mid-year, your REPS claim will rely partly on reconstructed hours from the period before you began logging. This introduces both opportunity and risk.

What you can reconstruct. Calendar entries showing property-related appointments. Emails and text messages with tenants, contractors, agents, and lenders. Bank statements showing property-related purchases. Contractor invoices with dates. Mileage records if you track them. Property management software logs. Showing schedules if you are an agent. Closing documents with timelines.

What limits reconstruction quality. The further back you go, the less you remember. Details that seem unforgettable in March become fuzzy by July. Specific activity descriptions give way to general estimates. And the IRS knows that a log created in July for January through June activities is not contemporaneous, no matter how well formatted it looks.

How to handle it honestly. If you reconstruct hours for the pre-tracking period, be transparent in your records. Note which entries are based on contemporaneous evidence (emails, calendar, receipts) and which are based on recollection. Conservative estimates supported by evidence carry more weight than aggressive estimates based on memory alone.

The Calendar Sync Advantage

One of the most powerful tools for recovering pre-tracking hours is your existing calendar. If you have been scheduling property visits, contractor appointments, tenant showings, or real estate meetings on your calendar, those entries serve as contemporaneous evidence of your activities.

A tracking system that can import calendar events gives you an immediate head start on recovering lost time. You are not fabricating entries; you are converting existing, timestamped records into a structured log format.

This approach has several advantages. First, calendar entries were created at or near the time of the activity, satisfying the contemporaneous requirement. Second, they typically include details like location, attendees, and purpose. Third, they are difficult to fabricate retroactively without leaving digital forensic traces.

The limitation is that your calendar probably does not capture every real estate activity. Unscheduled phone calls, spontaneous property visits, research time, and administrative work likely are not on your calendar. But the calendar entries provide a documented baseline that you can supplement with other evidence.

When the Math Just Does Not Work

There comes a point in the year when reaching 750 hours is not realistic given your actual real estate involvement. Recognizing this point honestly is important.

If you work a full-time W-2 job at 40 hours per week (approximately 2,080 hours annually), the more-than-half test means your real estate hours must also exceed 2,080, which effectively requires more than 2,080 hours of real estate activity. That is a second full-time job and then some. For most people with full-time non-real-estate employment, REPS is not achievable regardless of when they start tracking.

If you work part-time, the math becomes more favorable. A part-time job at 20 hours per week (approximately 1,040 hours annually) means you need more than 1,040 real estate hours to pass the more-than-half test, plus more than 750 for the absolute threshold. These numbers are achievable for someone deeply involved in real estate activities, but they still require genuine full-time-equivalent real estate work.

The honest assessment: if your real estate activities would not have exceeded 750 hours even if you had tracked from January 1, then starting mid-year does not change the outcome. You cannot track your way to qualification if the underlying hours were never there.

Alternatives If REPS Will Not Work This Year

If the math makes REPS infeasible for the current tax year, you have several alternative strategies worth discussing with your tax advisor.

Active participation exception. Even without REPS, you can deduct up to $25,000 in rental losses if you actively participate in rental activities and your adjusted gross income is below $150,000 (with phase-out beginning at $100,000). This does not require 750 hours or any specific hour threshold, though it does require meaningful involvement in management decisions.

Grouping election for future years. If you own multiple rental properties, filing a grouping election under Treas. Reg. Section 1.469-9(g) allows you to treat all of your rental activities as a single activity for material participation purposes. This can make it dramatically easier to meet material participation tests. The election is made on the tax return for the year it is first effective.

Carry-forward suspended losses. Rental losses you cannot deduct this year are not lost forever. They are suspended and carry forward to future years, where they can offset rental income or be fully deducted when you dispose of the property.

Prepare for next year. If you start tracking now, even knowing this year will not qualify, you build the habit and documentation system that will serve you next year. Starting January 1 with a proven tracking system and an established routine puts you in a much stronger position.

A Month-by-Month Action Plan

Here is a practical approach if you are starting mid-year and believe REPS qualification is still achievable.

Immediately. Set up a tracking system and begin logging every real estate activity in real time from today forward.

Week one. Gather all supporting evidence for the pre-tracking period: calendar entries, emails, text messages, bank statements, contractor invoices, receipts, and mileage records.

Weeks two and three. Reconstruct hours for the pre-tracking period using your supporting evidence. Be specific, honest, and conservative. Cross-reference multiple sources for each entry where possible.

Monthly. Review your running total against the 750-hour target. Calculate the weekly average you need for the remainder of the year. Adjust your documentation habits if you are falling behind.

Year-end. Compile your complete log, both reconstructed and contemporaneous sections, with supporting evidence organized and accessible.

Key Takeaways

- Starting mid-year is feasible if the math works. Through June, most full-time real estate professionals can still reach 750 hours with diligent tracking.

- The pre-tracking period requires honest reconstruction supported by contemporaneous evidence like calendar entries, emails, receipts, and bank statements.

- Calendar sync is your most powerful reconstruction tool because calendar entries were created at or near the time of the activity.

- After August, the math becomes extremely difficult without substantial reconstructed hours from earlier in the year.

- If REPS will not work this year, the active participation exception, loss carry-forwards, and preparation for next year are viable alternatives.

- Starting to track mid-year, even if this year does not qualify, builds the habits and systems you need for future years.

Frequently Asked Questions

Is there a deadline to decide whether to claim REPS?

No. REPS is claimed on your tax return, so the decision is made at filing time. You do not need to elect REPS status in advance. You can track hours all year and decide at tax time whether the numbers support a REPS claim.

Can I combine reconstructed hours and tracked hours in the same log?

Yes. A log that transitions from reconstructed entries (supported by evidence) to contemporaneous tracked entries is perfectly acceptable. In fact, this pattern is common because many people do not learn about REPS documentation requirements until after they have already been doing the work.

What if my real estate hours are close to 750 but I am not sure?

If you are in the gray zone (say, 700 to 800 hours), the quality of your documentation becomes even more critical. Borderline claims attract more scrutiny, and a well-documented claim at 760 hours is stronger than a poorly documented claim at 900 hours. Focus on making every logged hour defensible.

Does the IRS prorate the 750-hour requirement for new investors?

No. The 750-hour requirement applies to the full tax year regardless of when you started investing in real estate. If you bought your first property in September, you still need more than 750 hours for that calendar year. For most new investors in the second half of the year, REPS qualification for that first year is unrealistic.

Can I count hours from December of the prior year?

No. The 750-hour test is strictly calendar-year based, running from January 1 through December 31. Hours from the prior year count toward that year’s test, and hours from the current year count toward this year’s test. There is no carryover.

Should I track hours even if I am certain I will not qualify this year?

Absolutely. Tracking now accomplishes two things. First, it establishes your documentation system and daily habits so you are ready for January 1 of next year. Second, the hours you track may be relevant if your tax situation changes unexpectedly, such as leaving a W-2 job mid-year and suddenly meeting the more-than-half test.

What counts as “starting” to track hours?

Starting means you begin maintaining a contemporaneous record of your real estate activities with dates, descriptions, and time spent. There is no formal registration or notification required. You simply begin logging your work.

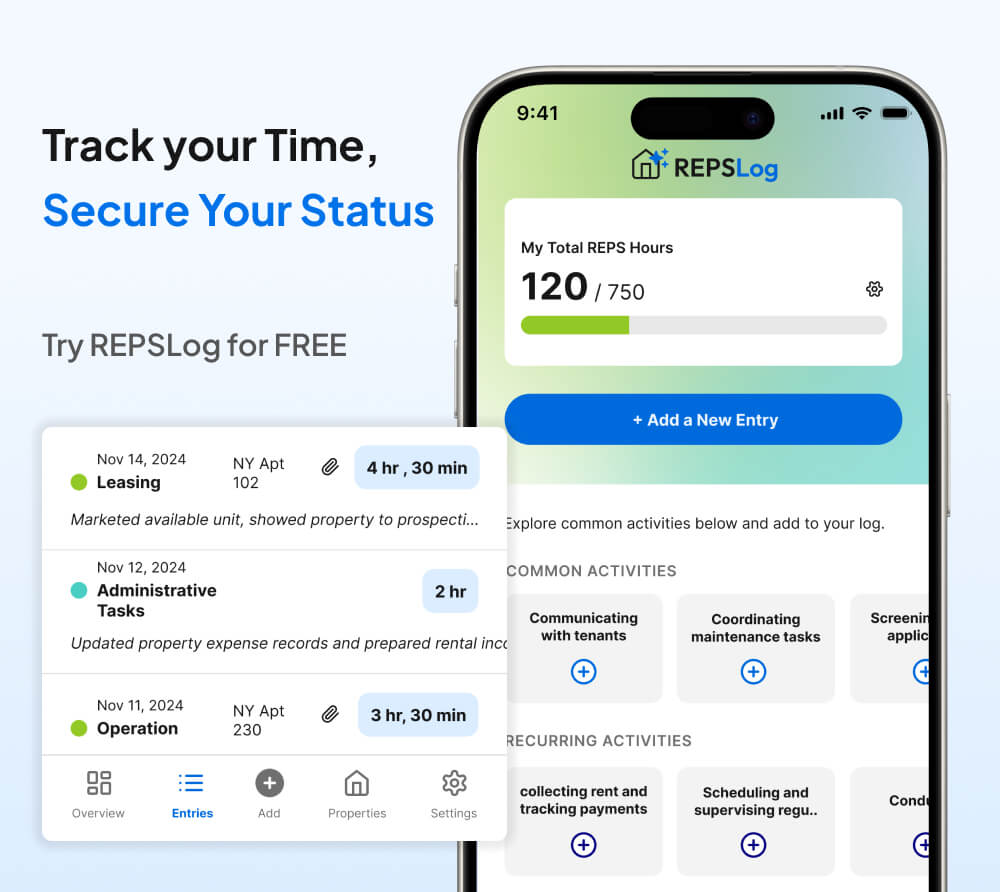

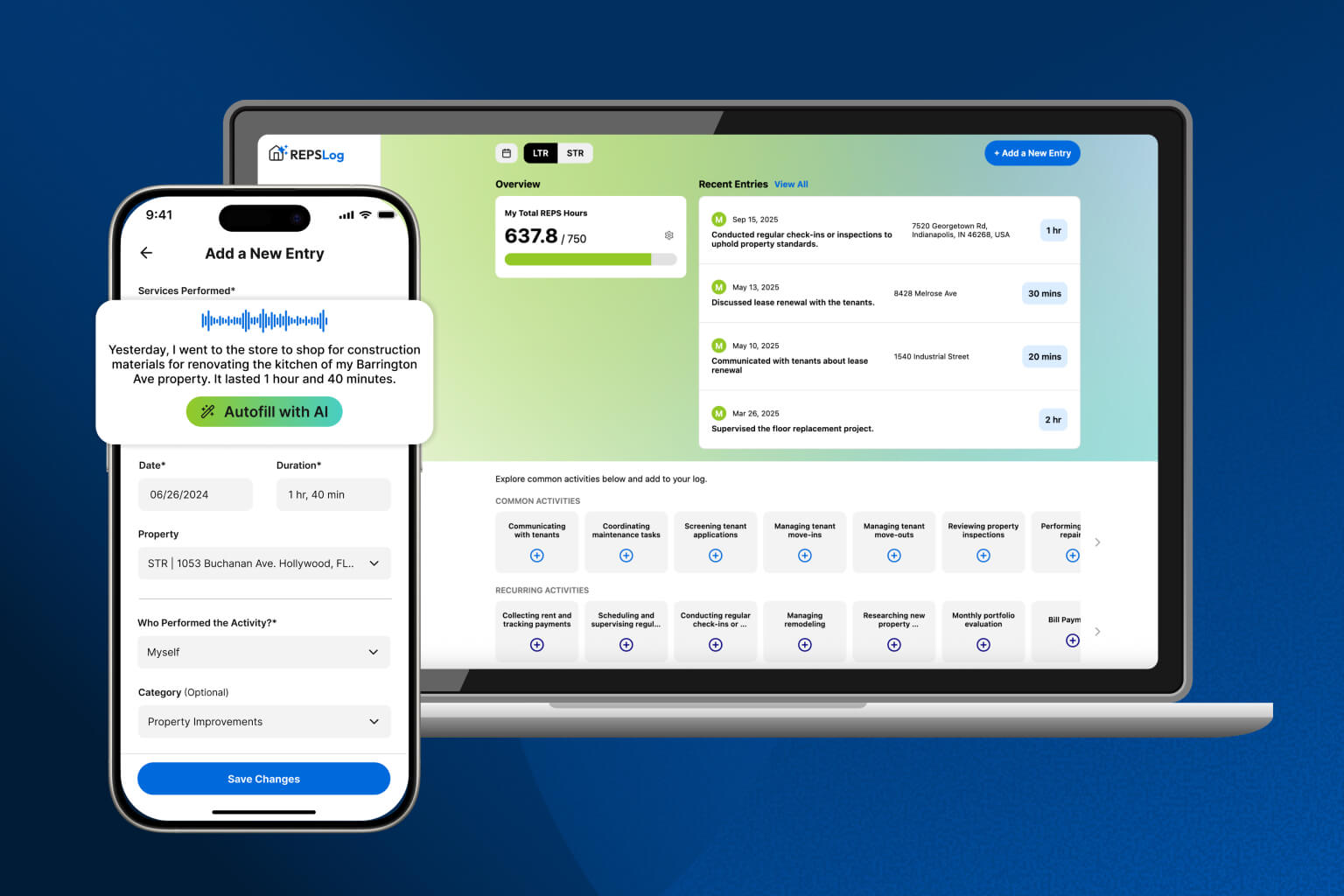

Whether you are starting fresh or recovering lost months, REPSLog makes it straightforward to build a defensible REPS log from wherever you are. Calendar sync helps you recover pre-tracking hours from your existing schedule, while real-time logging ensures every hour going forward is captured with the detail the IRS expects. Get started on iOS, Android, or Web.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance tailored to your situation.