“Just take a picture.” It is one of the most common pieces of advice in online real estate forums when someone asks how to document their REPS hours. And on the surface, it seems logical: a photo with a timestamp and geotag proves you were at a property at a specific time. Case closed.

Except it is not that simple. Photos can be a useful supplement to your REPS documentation, but they do not prove what most people think they prove. Relying on photos as your primary evidence of material participation is a strategy that has failed repeatedly in Tax Court.

This article explains what photos actually demonstrate, what the IRS requires under the applicable regulations, and how to build a documentation approach that uses photos correctly as part of a larger evidence strategy.

What Photos Prove

A photograph with embedded metadata (EXIF data) can establish several facts with reasonable reliability.

Location. If your phone’s GPS was active when you took the photo, the EXIF data records the coordinates where the photo was taken. This proves you were physically at or near a specific location.

Date and time. The timestamp in the photo metadata records when the image was captured, assuming your device’s clock was accurate.

Visual conditions. The photo shows what the property or work area looked like at that moment, including the state of construction, the presence of contractors or equipment, weather conditions, and so on.

These are genuinely useful data points. But notice what is missing from that list.

What Photos Do Not Prove

Duration of activity. A photo taken at 9:00 AM at your rental property proves you were there at 9:00 AM. It says nothing about whether you were there for 15 minutes or five hours. Even if you take a second photo at 2:00 PM, the two photos only prove you were at the property at two specific moments. You could have left and returned, or you could have been sitting in your car scrolling social media between photos.

Nature of participation. A photo of you at a property does not demonstrate what you were doing there. Were you actively inspecting plumbing work, negotiating with a contractor about change orders, and reviewing the project budget? Or were you dropping off your child who wanted to see the construction equipment? The photo cannot answer that question.

Quality of involvement. Even if a photo shows you standing next to a contractor on a job site, it does not establish whether you were directing the work, making decisions, inspecting quality, or simply observing. The Tax Court has drawn clear distinctions between active management and passive presence, and photos cannot capture that distinction.

Consistency over time. REPS requires more than 750 hours across the full year. Photos from a handful of property visits do not establish the kind of consistent, year-round involvement the IRS expects. A collection of 50 photos spread across 12 months shows 50 moments, not 750 hours of work.

What the IRS Actually Requires

Treasury Regulation 1.469-5T(f)(4) specifies the documentation standard for material participation. It calls for participation to be established by “any reasonable means,” which can include identifying services performed and the approximate number of hours spent on those services based on appointment books, calendars, or narrative summaries.

The regulation emphasizes three elements: the services performed (what you did), the time spent (how long), and the dates (when). A complete documentation system addresses all three. A photo addresses only the date and possibly the location, which is just one dimension of a three-dimensional requirement.

The IRS wants to see a log or similar document that records daily activities with enough specificity to evaluate whether the work constitutes material participation. The log should describe the activities in enough detail that an examiner can assess both the nature and the duration of the work. Photos do not provide this narrative.

How Photos Have Failed in Tax Court

Multiple Tax Court cases illustrate the limitations of photo-based REPS documentation.

In cases where taxpayers relied heavily on photos to support their participation claims, the court typically noted that photos confirmed the taxpayer visited the property but did not establish the duration of the visit, the nature of the work performed, or the hours spent on management activities. The photos corroborated location and date but left the most important questions, specifically what was done and for how long, unanswered.

Courts have been particularly skeptical when taxpayers presented photos as a substitute for, rather than a supplement to, detailed activity logs. A stack of property photos with no accompanying log of activities performed, time spent, and decisions made is essentially asking the court to infer participation from mere presence. Courts have consistently declined to make that inference.

The Right Way to Use Photos

Despite all of the above, photos are not worthless for REPS documentation. Used correctly, they serve as corroborating evidence that strengthens a well-maintained activity log. Here is how to use them effectively.

Pair every photo with a log entry. When you take a photo at a property, make a corresponding entry in your activity log that describes what you were doing, how long you spent, and what decisions you made. The photo confirms you were there; the log entry documents what you did.

Photograph specific work or conditions. Instead of generic property photos, capture specific items you inspected, issues you identified, or work you directed. A photo of a water stain on a ceiling, paired with a log entry about investigating the leak source and calling a plumber, tells a coherent story of active participation.

Use before-and-after sequences. Photos showing a property’s condition before and after your work demonstrate that something happened. Combined with log entries detailing the work you performed or managed between the two photos, the sequence becomes compelling evidence of active involvement.

Do not over-rely on them. Photos should be one layer in a multi-layer documentation system, not the foundation. Your primary evidence should always be a detailed, contemporaneous activity log. Photos add credibility to that log.

Building a Complete Documentation Strategy

The strongest REPS documentation combines multiple types of evidence, each covering different aspects of your participation.

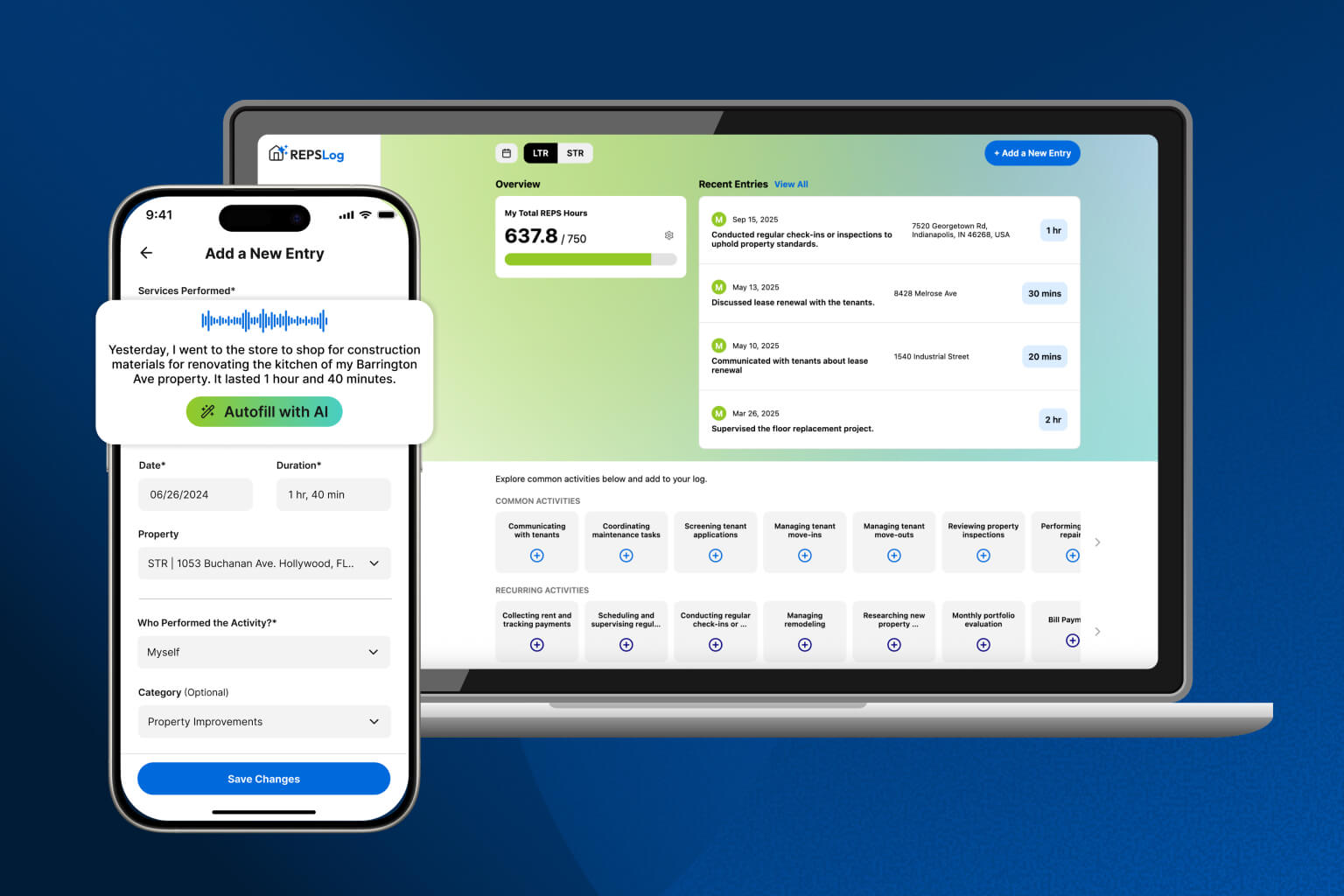

The activity log. This is your primary document. Every real estate activity gets an entry recording the date, the property, the activity description, the time spent, and any relevant notes. This log satisfies the core requirements of Treasury Regulation 1.469-5T(f)(4).

Communications. Emails, text messages, and phone records showing conversations with tenants, contractors, property managers, agents, and lenders. These prove you were actively managing relationships and making decisions.

Financial records. Bank statements, credit card statements, invoices, and receipts showing property-related expenditures. These corroborate the activities described in your log and demonstrate financial engagement with your properties.

Calendar entries. Appointments, meetings, showings, and inspections on your calendar serve as contemporaneous evidence of planned and executed activities.

Photos. Dated, geotagged photos of property visits, inspections, and work in progress serve as visual corroboration of your log entries.

Third-party records. Contractor invoices, property management reports, inspection reports, and tenant correspondence provide independent confirmation of your involvement.

The strength of this approach is that each type of evidence compensates for the weaknesses of the others. Your log provides narrative detail that photos lack. Your photos provide visual confirmation that a written log alone cannot offer. Your financial records provide objective evidence that neither logs nor photos can match.

When Photos Actually Help

There are specific scenarios where photographic evidence carries more weight than usual.

Documenting property conditions for insurance or repair purposes. If you photograph damage, deterioration, or maintenance needs, those photos combined with log entries about your response create strong evidence of active property management.

Recording self-performed work. If you personally paint rooms, install fixtures, repair fences, or perform other physical work on your properties, photos of you doing the work (or of the work in progress) combined with log entries are powerful evidence. The physical work is visible in the photo, and the log records the time spent.

Establishing regular presence patterns. A series of photos taken at consistent intervals (weekly property visits, for example) establishes a pattern of regular involvement that supports your log’s claim of ongoing participation. The photos do not prove what you did during each visit, but they confirm that the visits occurred as documented.

Before-and-after renovation documentation. For major renovation or development projects, a comprehensive photo timeline showing the project from demolition through completion, paired with detailed project management logs, creates a compelling record of sustained involvement.

Key Takeaways

- Photos prove location and date but do not prove the duration of your visit, the nature of your participation, or the quality of your involvement.

- The IRS requires documentation of services performed, time spent, and dates of work under Treasury Regulation 1.469-5T(f)(4). Photos address only the date dimension.

- Tax Court has consistently treated photos as supplementary evidence, not primary documentation of material participation.

- The most effective use of photos is as corroboration for a detailed, contemporaneous activity log. Pair every property photo with a corresponding log entry.

- Build a multi-layer documentation strategy combining activity logs, communications, financial records, calendar entries, photos, and third-party records.

- Photos of specific conditions, self-performed work, and project timelines carry more evidentiary weight than generic property snapshots.

Frequently Asked Questions

Can I use photos as my only form of REPS documentation?

This approach is extremely risky and has been rejected by Tax Courts. Photos alone do not satisfy the documentation requirements because they cannot establish the duration or nature of your participation. You need a detailed activity log at a minimum.

Do geotagged photos carry more weight than non-geotagged ones?

Geotagged photos are slightly more useful because they confirm both location and date rather than just date. However, the fundamental limitation remains: they prove where you were, not what you did or how long you spent doing it.

How many photos should I take per property visit?

There is no magic number. One or two purposeful photos that document specific conditions, work in progress, or decisions being made are worth more than 20 generic snapshots of the property exterior. Focus on quality and relevance over quantity.

Can the IRS challenge the authenticity of my photos?

Yes. The IRS can examine EXIF metadata to verify dates, times, and locations. They can also check whether metadata has been altered, whether photos have been digitally modified, or whether the same photo appears in multiple years’ documentation. Digital forensics can detect many forms of photo manipulation.

Should I include photos of myself at the property?

Photos showing you at the property can help establish your presence, but remember that your presence alone is not participation. If you include self-photos, pair them with log entries explaining what you were doing. A photo of you next to a contractor is more useful if accompanied by a log entry saying “Met with electrician to review panel upgrade scope; approved $4,800 estimate.”

Are screenshots of property management software considered photos?

Screenshots of property management dashboards, tenant portals, or maintenance request systems are a different category of evidence. They can demonstrate active engagement with management activities and are generally more useful than property photos because they show you doing property management work, not just being at a property.

What about video evidence? Is that better than photos?

Video can be marginally better because it can capture conversation, show you actively participating in discussions or inspections, and demonstrate duration more than a single photo. However, video still needs to be paired with log entries and carries the same fundamental limitation: it shows moments, not full-day activity patterns.

Photos supplement your REPS documentation but cannot replace the detailed, contemporaneous activity log that the IRS expects. REPSLog helps you maintain the kind of structured, detailed records that stand up to IRS scrutiny, with categorized activities, time tracking, and property-level organization that gives your documentation the depth photos alone cannot provide. Available on iOS, Android, or Web.

This article is for educational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance tailored to your situation.